If you want to understand what’s really happening in crypto, sometimes the best place to look isn’t price charts or Twitter threads — it’s the exchanges. A major publicly traded exchange just published a Q2 shareholder letter that pulled back the curtain on trading behaviour, revenue trends, product traction, and strategic bets that will shape the next phase of crypto adoption. I went through the numbers, the surprises, and the guidance, and in this deep-dive I’ll walk you through what the report actually reveals about the health of crypto today and what to watch for next.

Table of Contents

- What this article covers

- Quick refresher: Who is this exchange and why should you care?

- How Coinbase makes money — the main engines

- What analysts expected heading into the Q2 report

- What actually showed up: the Q2 numbers (the headline read)

- Beyond the numbers: product momentum and strategic traction

- Q3 outlook: cautious optimism with increased investment

- What this all means for crypto — the big takeaways

- What investors, users, and builders should watch next

- Dealing with the one-offs: understanding the adjusted picture

- How to interpret the result if you’re a retail investor

- Risks and counterpoints

- FAQ — Frequently asked questions

- Final thoughts — the larger narrative

- Parting note

What this article covers

- A clear breakdown of how the exchange makes money today (fees, subscriptions, custody, USDC, Base, and more)

- What analysts were expecting heading into Q2 and why their views diverged

- Exactly what showed up in the Q2 results: revenue, trading volumes, custody milestones, and one-off costs

- How Coinbase’s Q3 outlook frames the short-term trajectory

- Strategic moves that matter (Base adoption, product rollouts, Deribit acquisition)

- Practical takeaways for the broader crypto market and what metrics to watch

- Answers to the most common FAQs about the results and implications

Quick refresher: Who is this exchange and why should you care?

Coinbase was founded in 2012 by Brian Armstrong and Fred Ehrsam and has grown into one of the largest crypto exchanges in the United States and a top-ten player globally. Fred stepped away in 2017, but Brian remained at the helm and steered the company through rapid product expansion and heavy regulatory focus. Its popularity came first and foremost from ease-of-use — a clean UI, a frictionless onboarding experience, and a product designed to appeal to mainstream users.

Today, Coinbase reports roughly 8.7 million monthly transacting users and operates far beyond a simple buy/sell order book. It’s a diversified crypto company with multiple revenue streams: transaction fees, subscriptions and services, custody and institutional services, staking and rewards, interest and financing, and strategic investments like its stake in Circle (the issuer of USDC). Because Coinbase is publicly traded, we get a clear look into how these businesses are performing — which makes every quarterly letter extremely useful for reading the state of the broader crypto market.

How Coinbase makes money — the main engines

Let’s unpack the big revenue lines so the Q2 figures make sense.

1) Transaction fees (trading revenue)

This is the classic exchange business: fees charged when users buy, sell, or trade crypto. Coinbase’s fees are generally higher than many competitors. There are two main reasons for that:

- Ease and trust: Many retail users are willing to pay a premium for a smoother UX and the security of a well-known brand.

- Regulatory compliance: Coinbase spends heavily on legal, compliance, and regulatory processes. That cost ultimately flows through to the fees it charges.

2) Subscriptions and services

These are recurring or semi-recurring revenue streams that offer a more stable base under the business. They include:

- Coinbase One and Coinbase One Basic subscription tiers — which bundle perks like zero trading fees and access to special cards.

- Coinbase Earn and staking services, where Coinbase takes a cut of staking rewards.

- Coinbase Wallet-related indirect revenues and in-app services.

3) Custody and institutional services

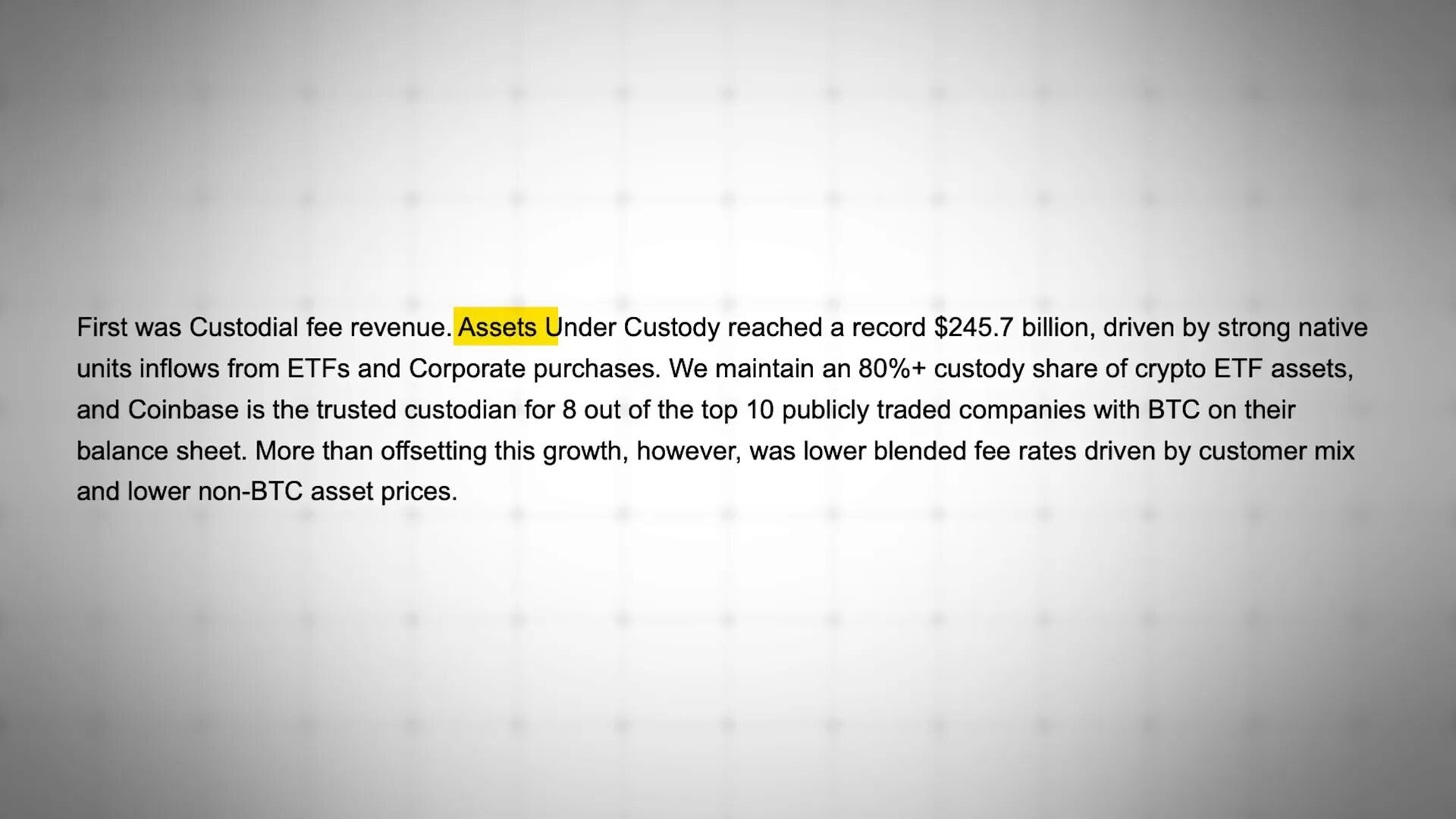

This is a huge business. Coinbase offers custodial services for institutions, funds, and ETFs. When institutions need safe, compliant custody, they frequently turn to big regulated custodians. As of Q2, Coinbase was stewarding $245.7 billion in assets under custody — an all-time high and a sign of significant institutional trust.

4) USDC partnership with Circle

This is one of the most interesting recurring revenue stories. Coinbase originally co-managed USDC with Circle in a 50/50 partnership until August 2021. Since then, Circle took operational control, but Coinbase kept revenue-sharing from the USDC reserves plus an equity stake in Circle (~8.5 million shares). Those reserves are primarily invested in high-quality, short-duration government bonds which are generating around ~5% yields in the current market environment. For Q2 alone, Coinbase reported roughly $332.5 million in revenue from this USDC reserve arrangement — a substantial and surprisingly stable revenue line.

5) Base — Coinbase’s Ethereum layer 2

Base is Coinbase’s L2 on Ethereum designed for cheap, near-instant transactions. Since launching, Base has seen more than $12 billion in assets moved on-chain and consistently processes billions in monthly transactions. It’s cheap to use — transaction costs are fractions of a cent — and increasingly functional, with integrations and a developer ecosystem building on top of it. Base is a strategic bet: lower transaction costs and fast UX can help drive on-chain activity, payments, and product innovation tied to Coinbase’s ecosystem.

What analysts expected heading into the Q2 report

Analysts were split heading into the earnings release because they were trying to reconcile declining trading activity with strengthening subscription and stablecoin revenue. The consensus from FactSet was about $1.59 billion in total revenue and EPS of $1.25 — clearly down from roughly $2 billion in Q1 but still above year-ago levels.

Here are some notable analyst views that shaped market expectations:

- Benjamin Budish (Barclays): Expected transaction revenue to fall due to weak retail trading activity, drawing parallels with Robinhood where retail volumes dropped roughly 43% QoQ. Yet he raised his price target from $202 to $359 on legislative optimism around stablecoin and digital asset clarity, even while keeping a neutral rating.

- Peter Christiansen (Citi): More bullish — raised his price target to $505 and reiterated a buy rating. He emphasized Coinbase’s inclusion in the S&P 500 and the potential upside from the stablecoin business, Base adoption, and subscription growth.

- Kenneth Worthington (JPMorgan): Balanced view — neutral rating and a $404 target. Acknowledged the strength in stablecoin-related revenue but flagged regulatory risk, compliance costs, and the lingering impact of cybersecurity incidents.

In short, the market narrative was optimistic overall, with upside potential driven by legislative clarity and long-term structural shifts, even if short-term transaction revenue looked shaky.

What actually showed up: the Q2 numbers (the headline read)

Coinbase published its Q2 shareholder letter on July 31. Here are the headline metrics and what they mean.

Top-line revenue

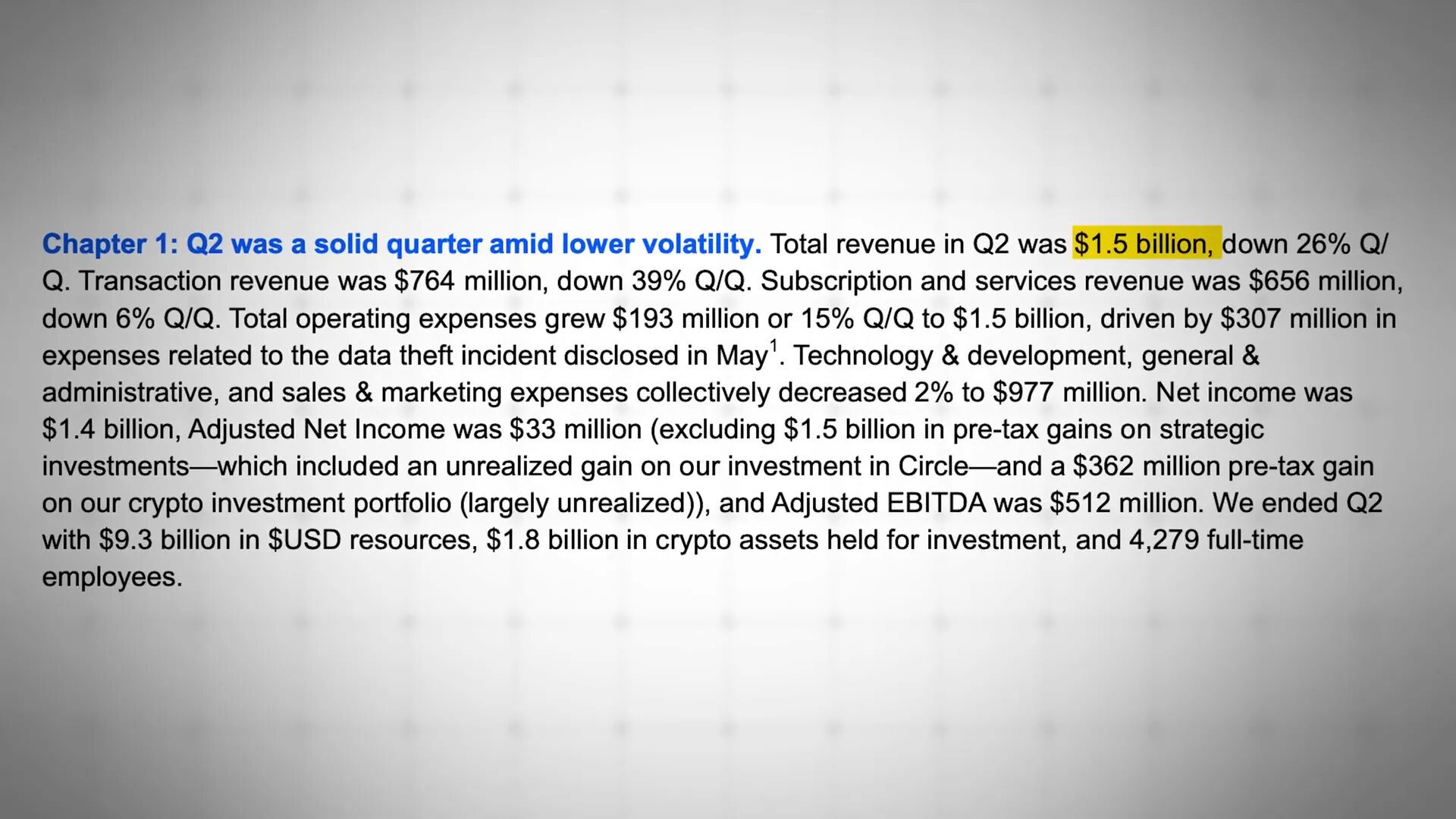

Total revenue in Q2: $1.5 billion, a 26% decline quarter-over-quarter. The major driver was transaction revenue falling sharply.

Transaction revenue and trading volumes

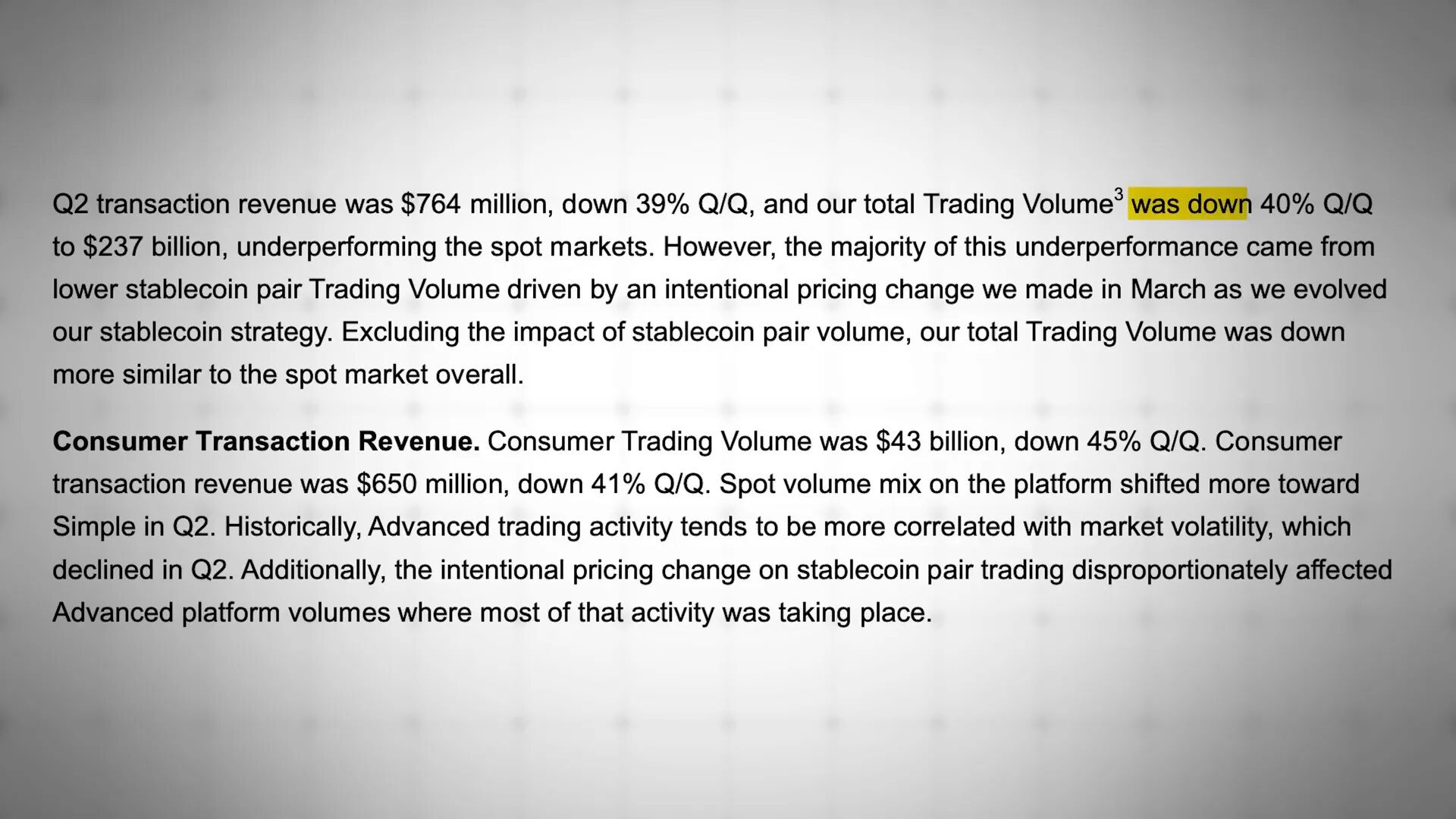

- Transaction revenue in Q2: $764 million, down 39% QoQ.

- Total trading volume: $237 billion, down ~40% QoQ.

- Consumer trading volume: $43 billion, down 45% QoQ (this partly reflects Coinbase’s deliberate pricing tweaks for stablecoin pairs implemented in March).

- Institutional trading volume: $194 billion, down 38% QoQ — more closely aligned to broader market conditions.

The drop in transaction revenue was attributed by Coinbase to significantly reduced crypto volatility and lower retail trading activity. Importantly, Coinbase highlighted that pricing changes to stablecoin trading pairs were a direct contributor to the revenue decline. When you remove volatile speculative retail activity and adjust trading fees downward on stablecoin pairs, you will naturally see a large revenue impact even if trading still occurs.

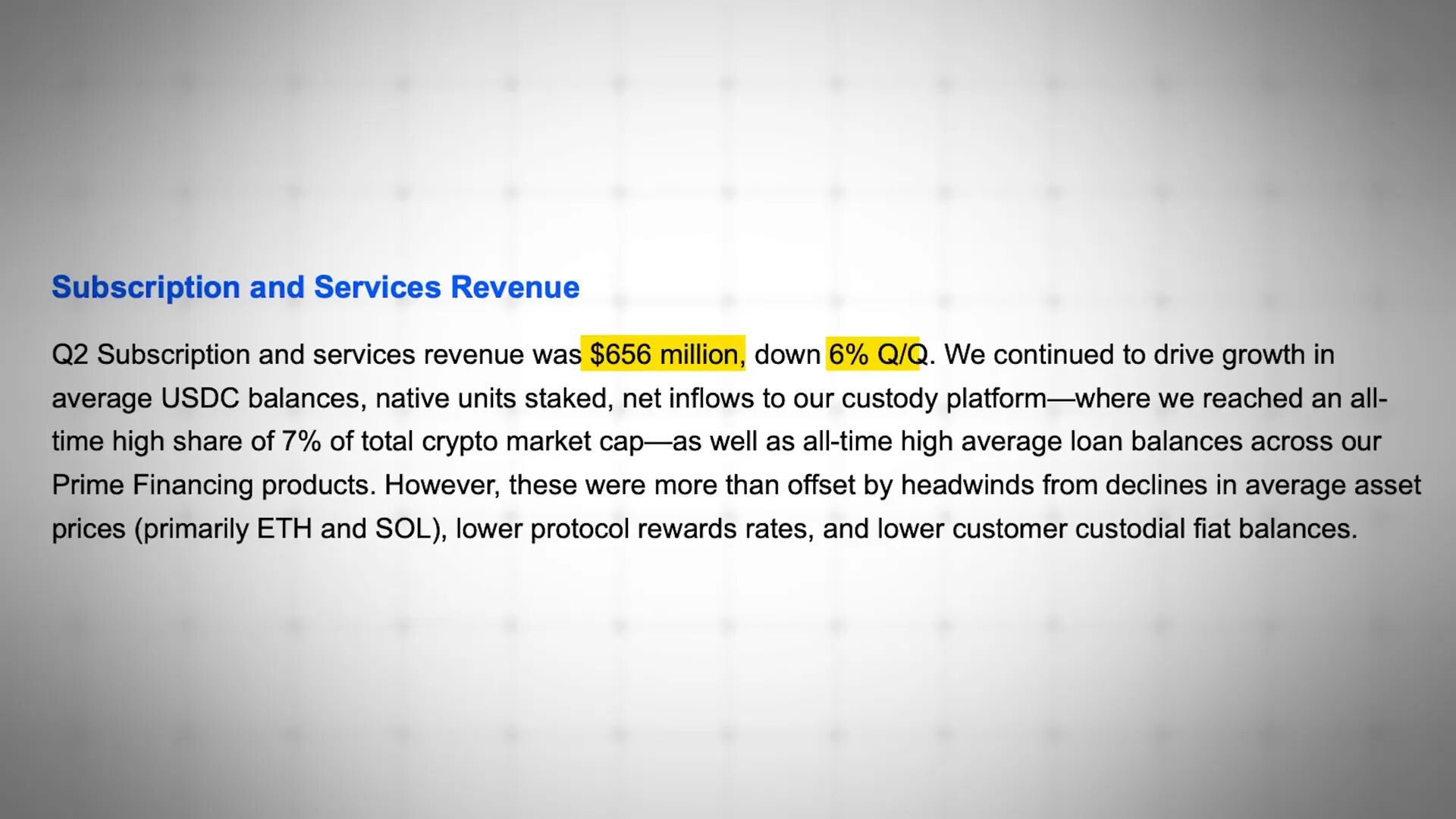

Subscriptions & services: relative stability

Subscription and services revenue was much more resilient: $656 million, a relatively modest 6% QoQ decline. The standout within this bucket was USDC-related revenue.

- USDC revenue: $332 million, up 12% QoQ. This was driven by higher average USDC balances held by users — average USDC balances increased 13% QoQ to $13.8 billion.

- Staking (blockchain rewards): $145 million, down 26% QoQ — mainly due to lower average prices for ETH and SOL and lower protocol reward rates.

- Interest & financing fee income: $59 million, down 6% QoQ (partially offset by record-high balances in prime financing driven by institutions like hedge funds and miners).

Custody milestone

Assets under custody hit an all-time high: $245.7 billion, representing more than 7% of the total crypto market capitalization. Coinbase remains the dominant custody provider for crypto ETFs in the U.S., holding over 80% of U.S. Bitcoin and Ethereum ETF assets.

Cybersecurity breach and one-time expenses

One of the quarter’s biggest headlines — and a key driver of cost — was a cybersecurity breach reported in May. Coinbase recorded significant one-time expenses tied to that event:

- One-time breach-related expenses: $307 million (customer reimbursements, legal and related expenses).

- As a result, total operating expenses increased 15% QoQ to about $1.5 billion.

Excluding those extraordinary costs, Coinbase actually reduced expenses in key areas: General & Administrative was down 10% and Sales & Marketing down 4% QoQ. Technology & Development spend, however, rose 9% as Coinbase continues to invest in product and engineering.

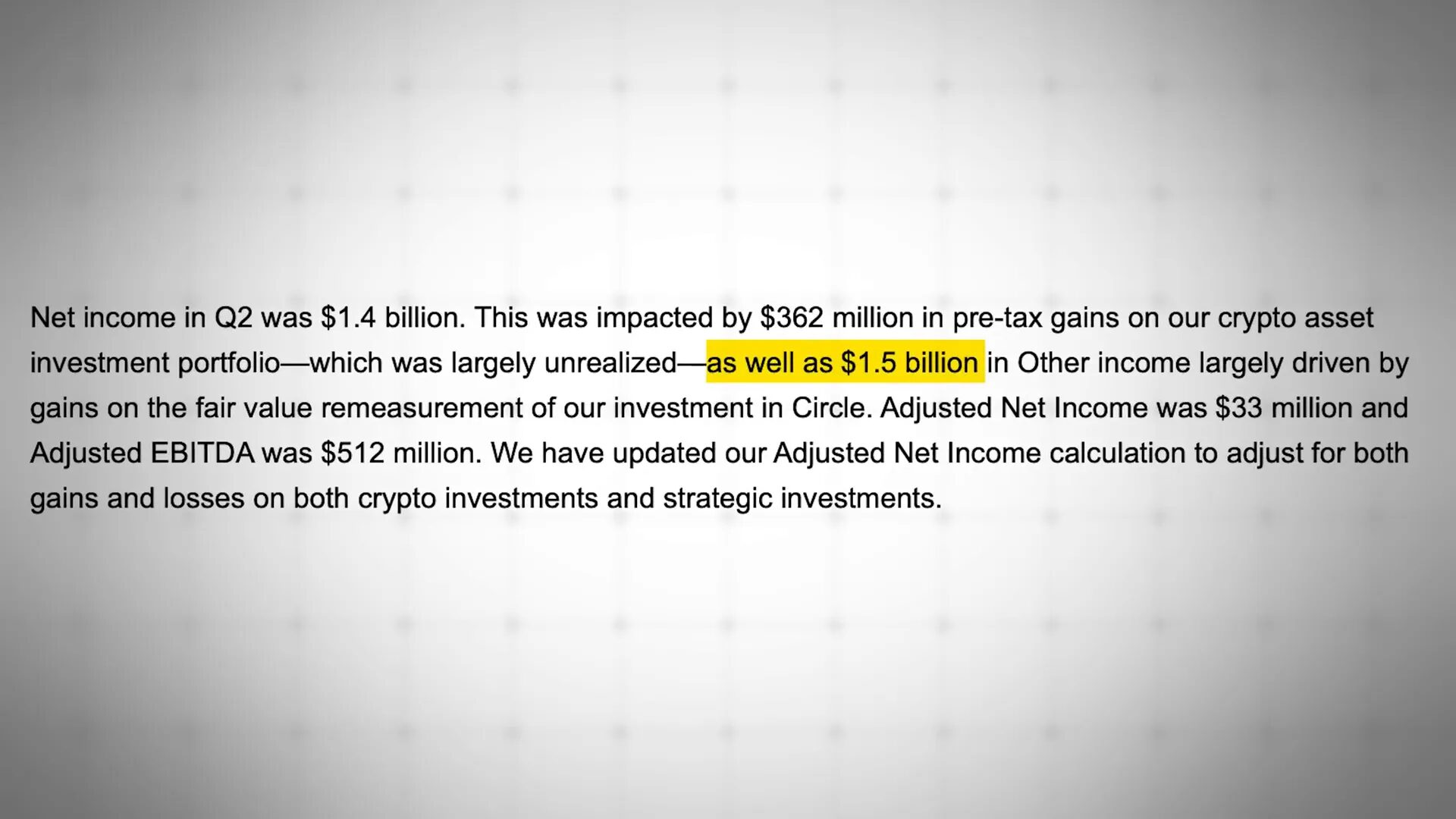

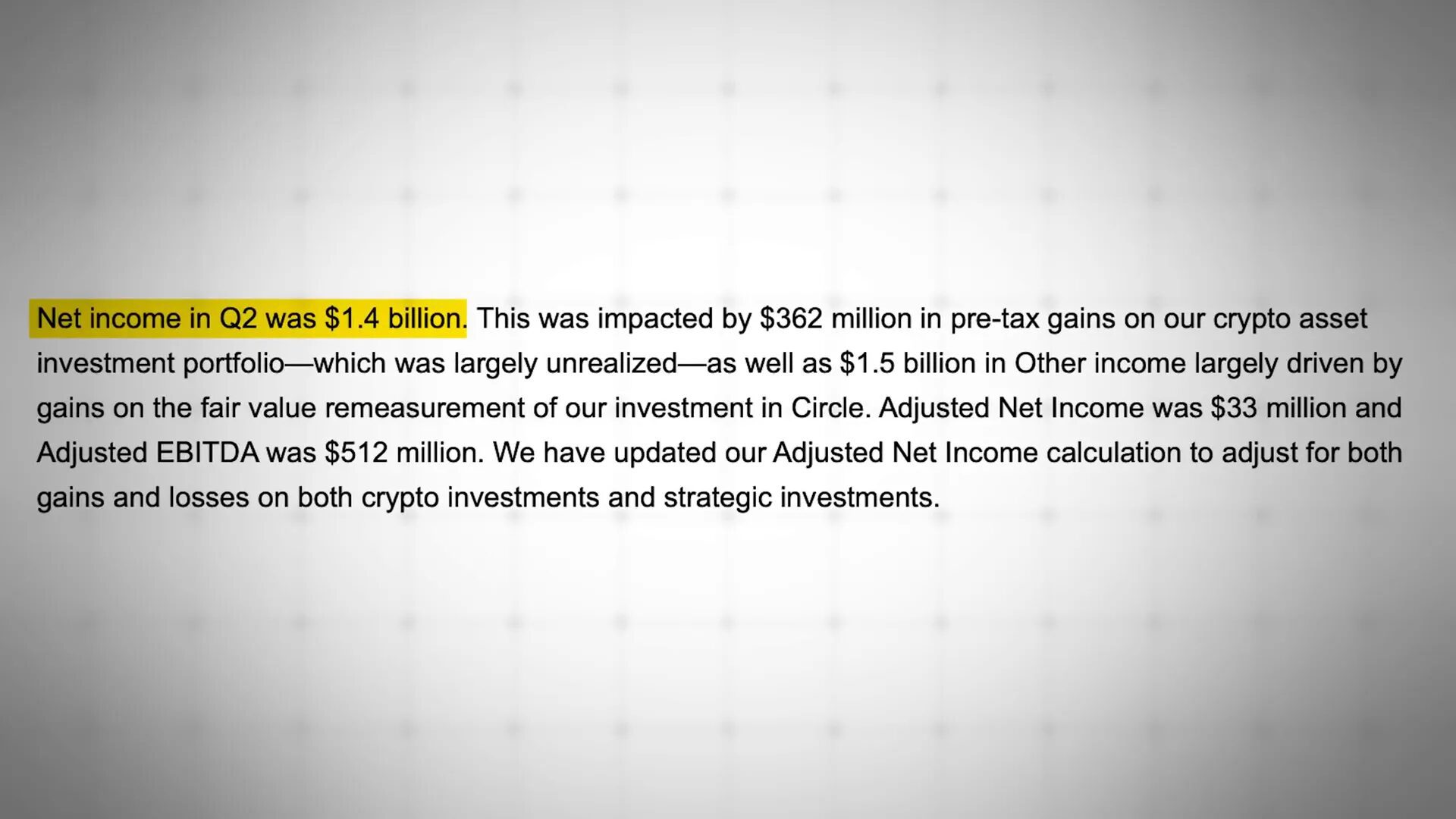

Net income and unrealized gains

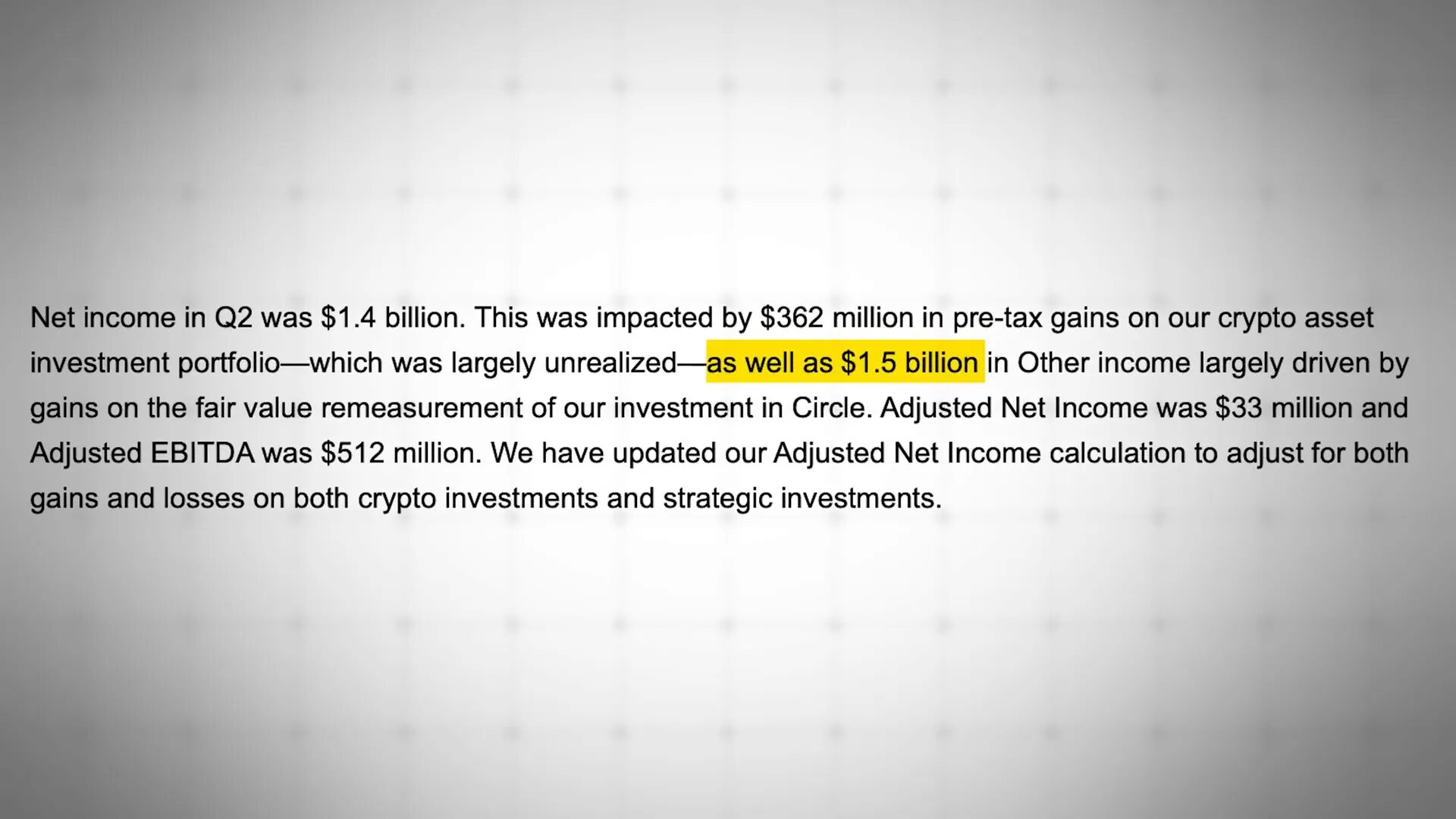

Coinbase reported a surprisingly high net income of $1.4 billion for the quarter — but most of that was driven by significant unrealized gains, not core operational profitability:

- Unrealized gain from Coinbase’s investment in Circle: $1.5 billion.

- Unrealized gain from Coinbase’s crypto asset portfolio: $362 million.

When you strip out these one-off or non-cash items and one-time expenses, Coinbase’s adjusted net income (which better reflects core operating performance) was a modest but positive $33 million.

Beyond the numbers: product momentum and strategic traction

It wasn’t all about revenue dips. Several product and strategic metrics suggest that Coinbase is building long-term optionality.

Base adoption is accelerating

Base continues to see strong on-chain activity: lightning-fast transaction times (measured in milliseconds) and transaction costs that can be fractions of a cent. The chain has moved more than $12 billion worth of assets since launch and processes billions in monthly transactions. These are not trivial numbers — they show there is persistent demand for low-cost, scalable L2 infrastructure even when markets are not euphoric.

Base app and on-chain experiences

Coinbase launched a Base app — a unified on-chain platform for social interactions, payments, and trading — and the waitlist blew past expectations: more than 700,000 sign-ups shortly after beta launch. That indicates real curiosity and potential user demand for on-chain products that blend social and financial interactions.

Consumer product expansion

Coinbase is expanding consumer offerings to attract and retain retail users: a more affordable Coinbase One tier, the Coinbase One card powered by American Express with up to 4% Bitcoin cashback for subscribers, and other retention features. These are designed to reduce reliance on pure transaction fees and lock users into subscriptions and product ecosystems.

Q3 outlook: cautious optimism with increased investment

Coinbase’s shareholder letter laid out a guardedly optimistic roadmap for Q3. The company is forecasting a modest revenue rebound but also expects higher operating costs due to deliberate investment in growth and compliance.

Revenue guidance

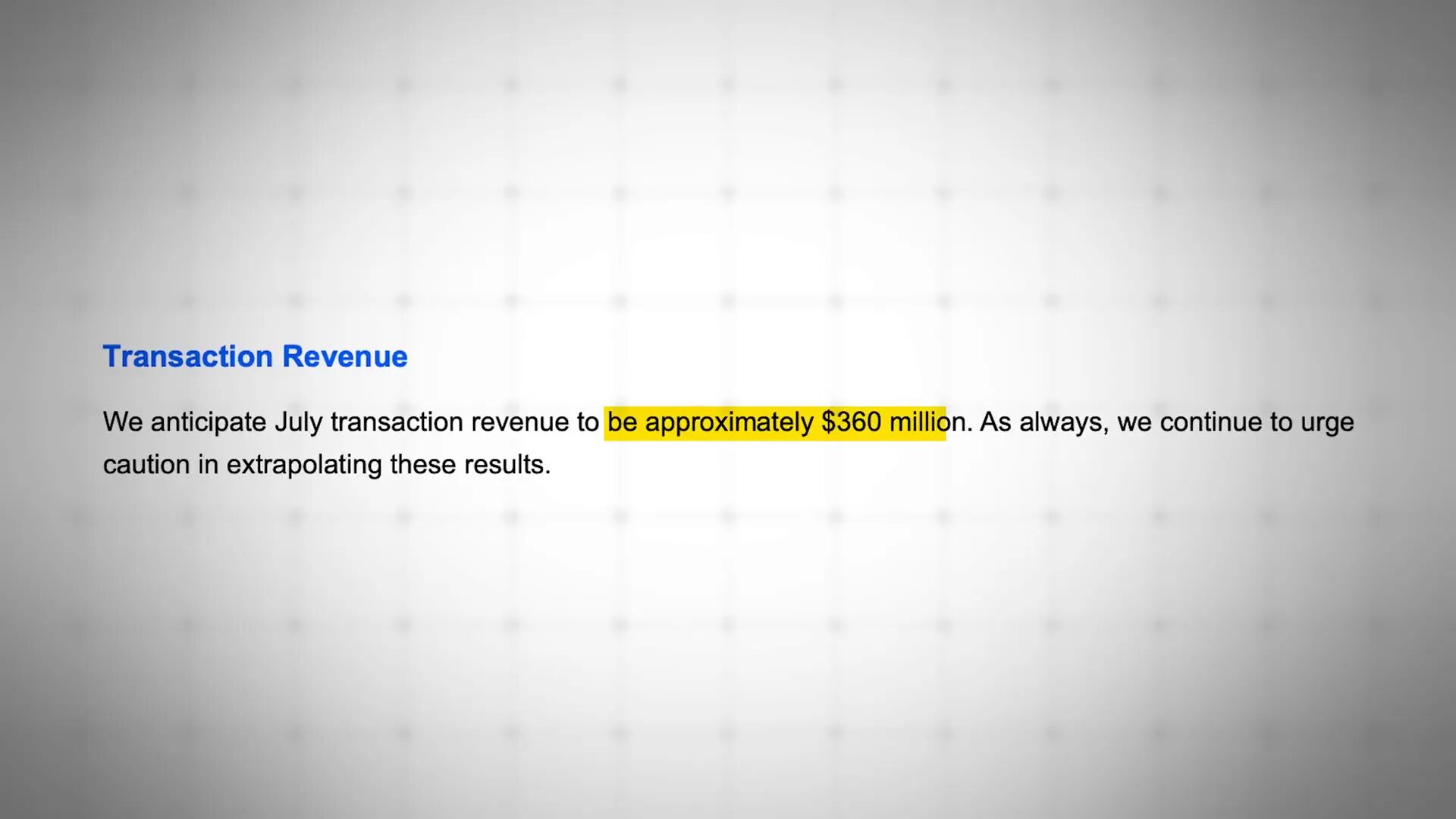

- Transaction revenue: Coinbase estimated July transaction revenue around $360 million, an improvement relative to the Q2 monthly average.

- Subscriptions & services: projected to rebound to between $665 million and $745 million, with much of the upside tied to higher average crypto prices.

- Stablecoin revenue: expected to grow further given USDC’s market cap hitting all-time highs in July.

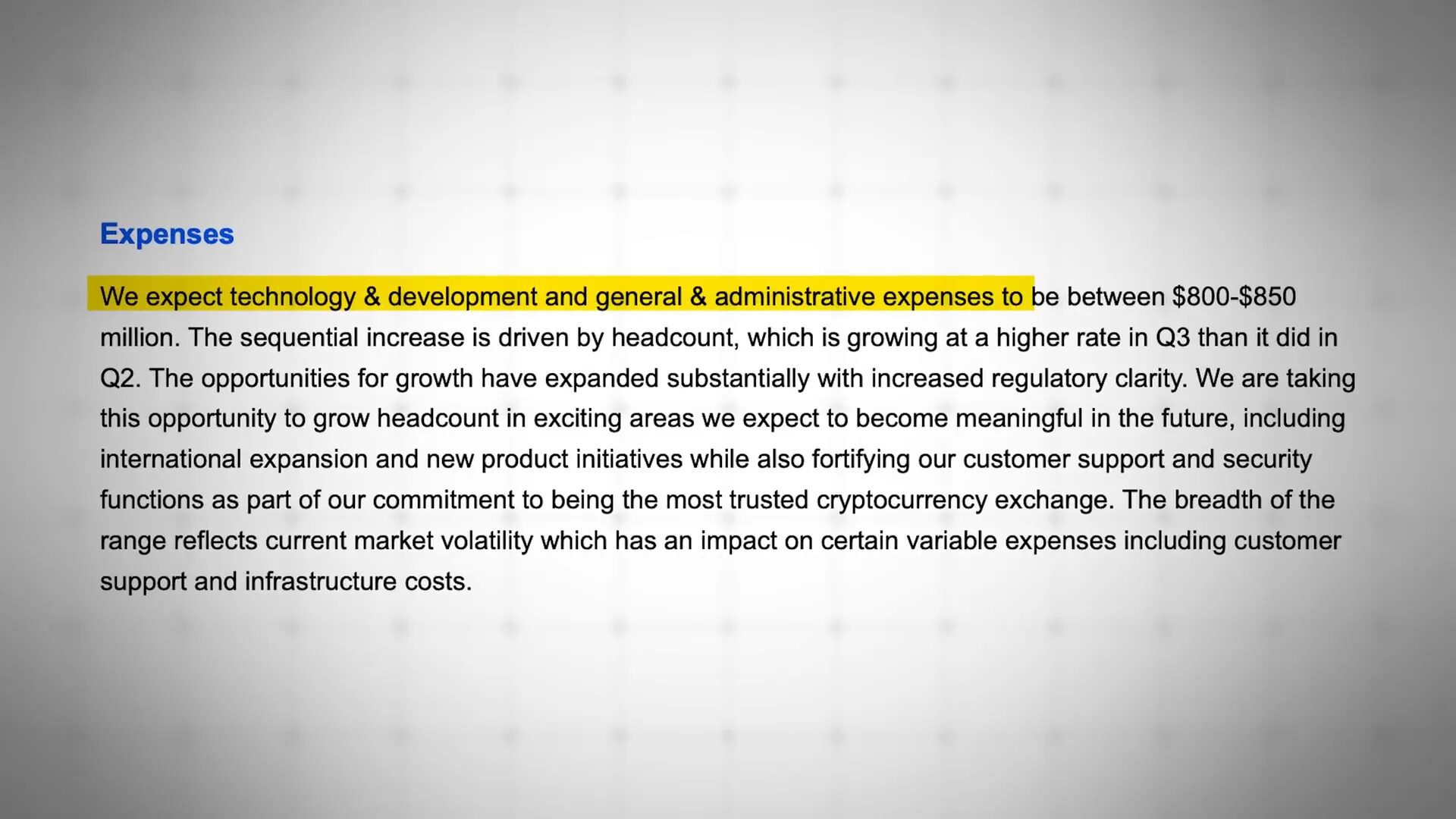

Expense guidance and headcount growth

Coinbase warned that expenses will increase in Q3 as it ramps hiring and invests in international expansion and regulatory initiatives:

- Technology & development plus General & Administrative: expected to be $800–$850 million.

- Sales & Marketing: expected to be $190–$290 million, with a wide range reflecting performance marketing opportunities that correlate with crypto volatility.

The company highlighted that S&M spend could swing materially depending on performance marketing opportunities (which are volatility-dependent) and changes in USDC balances (which impact reward payouts and costs).

Strategic acquisition: Deribit

Coinbase is preparing to close the acquisition of Deribit, a major crypto options and derivatives platform, expected by December 2025. This deal would deliver several strategic benefits:

- Broaden Coinbase’s derivatives and options product suite.

- Improve international footprint in derivatives trading.

- Potentially deliver steadier revenue streams via options trading and institutional flows.

What this all means for crypto — the big takeaways

Reading an exchange’s books is one of the best ways to understand real activity in crypto. Here’s what Coinbase’s Q2 report tells us about the broader market and where things might head next.

1) We’re in a transitional market

Transaction volumes dropped sharply in Q2—especially retail trading volumes—but subscription services, stablecoin adoption, and custody traction were resilient. That suggests a shift away from short-term speculative retail activity and toward foundational use cases: payments, custody, staking, and stablecoin liquidity.

This is arguably healthier: exchanges leaning less on retail trading spikes and more on recurring revenue (subscriptions, USDC yields, custody) create a more sustainable business model and reduce the boom/bust sensitivity that characterized earlier years.

2) Stablecoins are a powerful and stable revenue engine

The USDC arrangement is a standout story. Coinbase’s revenue from USDC reserves ($332M in Q2) is essentially a margin on the yield from government bonds backing the stablecoin. As long as those reserves remain substantial and yields on short-duration treasuries remain attractive, stablecoin-related revenue is likely to be a consistent tailwind.

Watch USDC balances as a core signal: increasing average USDC holdings directly drive stablecoin revenue and can materially affect Coinbase’s subscription & services revenue line.

3) Product and on-chain adoption is progressing even in down markets

Base and on-chain products are gaining users and movement even during quieter trading periods. That demonstrates latent demand for low-cost L2 infrastructure. If Base continues to grow its developer and user ecosystem, it could be a structural growth lever for Coinbase — driving transactions, payments use cases, and new on-chain products.

4) Regulatory clarity is a major tailwind

Policy progress like the Genius Act (stablecoin clarity) and momentum behind the Clarity Act create a more predictable environment for regulated players such as Coinbase. Legislative clarity reduces uncertainty, promotes institutional adoption, and encourages mainstream financial firms to provide crypto offerings. That’s a major reason some analysts raised price targets despite near-term softness in trading revenue.

5) Macro liquidity, not just rate policy, drives crypto

While the Fed’s path matters, crypto rallies have historically been driven less by interest-rate policy per se and more by available liquidity, investor attention, and flows (including stablecoin-driven liquidity). Even without a rate cut, liquidity injections from other channels — Treasury bond buybacks, stablecoin issuers purchasing bonds, or increased institutional allocations — can create favourable conditions for crypto appreciation.

6) TradFi participation validates the ecosystem

Major traditional finance firms entering the crypto trading and custody business is a validation signal. These entrants bring distribution, capital, and credibility — expanding market depth and potentially smoothing liquidity across market cycles. Coinbase’s dominance in custody for ETFs tells a story of institutional trust that will likely attract more TradFi activity.

What investors, users, and builders should watch next

Here are the practical metrics and signals I’ll be tracking that will tell us whether the positive structural story is translating into growth:

- Trading volumes — consumer vs institutional: Consumer volumes indicate retail appetite; institutional volumes show deeper market participation.

- Transaction revenue trends: Are fee revenues stabilising or continuing to fall as Coinbase shifts pricing on stablecoins?

- Average USDC balances: Growth here is directly correlated with stablecoin revenue.

- Assets under custody (AUC): Expansion in custody reflects institutional trust and product adoption (ETF custody is particularly important).

- Base transaction metrics and developer activity: Increasing on-chain activity and developer deployments are long-term growth indicators.

- Subscription growth (Coinbase One tiers): Subscription take-rates and churn will show whether users stick around for recurring fees and perks.

- Expense trajectory and hiring: Watch how quickly operating expenses grow relative to revenue — this will affect adjusted profitability.

- Regulatory developments: New rules or clarifications can materially change custody, payments, and product offerings.

- Deribit acquisition progress: Closing the deal and integrating derivatives capability could add a more predictable revenue stream.

Dealing with the one-offs: understanding the adjusted picture

Q2 was complicated by a mix of recurring wins and one-time setbacks. That’s why it’s important to separate headline net income — which was boosted by unrealized, non-cash gains — from adjusted net income, which removes unusual items to show core operational health.

Key reconciliations to keep in mind:

- Unrealized gains from equity stakes (e.g., Circle) and crypto holdings can swing GAAP net income materially from quarter to quarter.

- One-time operating expenses (e.g., cybersecurity reimbursements and legal costs) can temporarily inflate operating expenses.

- Adjusted metrics (adjusted EBITDA, adjusted net income) are more useful when assessing ongoing profitability.

How to interpret the result if you’re a retail investor

If you’re an investor (and not a trader), here’s the lens I’d recommend:

- Focus on recurring revenue: Stablecoin yields, custody fees, subscriptions, and institutional services create a financial backbone that’s less volatile than trading fees.

- Watch cadence of product adoption: Base, Coinbase One, custody wins, and card adoption are forward-looking growth indicators.

- Understand volatility: Short-term price action and trading volume can swing revenue wildly — that’s why long-term investors should prioritise structural metrics over quarter-to-quarter trading revenue volatility.

- Factor in regulatory risk: Even with legislative progress, regulatory outcomes can rapidly change business dynamics — monitor legal developments closely.

Risks and counterpoints

It’s not all sunshine. Important risks remain:

- Regulatory uncertainty: While recent bills have been supportive, regulatory frameworks can shift across jurisdictions and enforcement can remain aggressive.

- Security and operational risk: The May cybersecurity breach demonstrated that even large, mature players can face costly incidents.

- Fee pressure: Competition on fees and deliberate pricing changes (e.g., stablecoin pair fees) can shave transaction revenue.

- Macro volatility: Liquidity shocks or broader market sell-offs can quickly reduce trading volume and revenue.

FAQ — Frequently asked questions

Q: Why did Coinbase’s total revenue fall in Q2?

A: The main cause was a sharp decline in transaction revenue (trading fees) — down 39% QoQ — driven by lower crypto volatility and significant declines in retail trading volumes. Coinbase also intentionally reduced stablecoin pair fees earlier in the year which further reduced revenue from those pairs, even as volumes continued to move on-chain.

Q: What is driving the growth in USDC revenue?

A: Coinbase benefits from revenue-sharing related to USDC reserves (invested in short-duration government bonds). In Q2, average USDC balances rose ~13% QoQ to $13.8 billion, which translated into higher reserve income. With short-duration Treasuries yielding ~5% in the prevailing environment, the interest earned on those reserves contributes materially to Coinbase’s subscriptions & services revenue.

Q: How meaningful were the one-time cybersecurity costs?

A: Very meaningful. Coinbase incurred about $307 million in one-time breach-related expenses for customer reimbursements and legal fees. These events increased total operating expenses by 15% QoQ. Excluding these costs, Coinbase actually reduced several expense categories, showing core cost discipline.

Q: Did Coinbase actually make money in Q2?

A: Yes on a GAAP basis Coinbase reported a net income of $1.4 billion; however most of that was driven by unrealized gains (notably $1.5 billion from its investment in Circle). The company’s adjusted net income, which strips out unrealized gains and one-offs, was a modest $33 million — reflecting a company near break-even on core operations but with clear structural revenue streams.

Q: What’s Base and why does it matter?

A: Base is Coinbase’s Ethereum Layer-2 scaling solution. It provides near-instant transactions at very low fees and has already seen billions of dollars moved on-chain. Base matters because it can drive on-chain activity, product innovation, and payments — all of which translate to long-term revenue potential for Coinbase as it builds an ecosystem around the chain.

Q: How will the Deribit acquisition change Coinbase’s business?

A: Deribit is a major crypto options and derivatives exchange. Acquiring Deribit could add a diversifying revenue stream from options trading, expand Coinbase’s international derivatives footprint, and attract institutional flows. The deal is expected to close by December 2025 and should be watched for regulatory approvals and integration plans.

Q: Should I buy Coinbase stock based on this quarter?

A: I can’t provide financial advice. What I will say is that the quarter shows a company transitioning from volatile fee-dependent income toward more diversified, recurring revenue streams (stablecoin income, custody, subscriptions). Your decision should weigh the valuation, your time horizon, risk tolerance for regulatory and security events, and belief in the long-term adoption of crypto.

Q: Which metrics should I watch each quarter?

A: Monthly transacting users, total and segmented trading volume (retail vs institutional), transaction revenue, subscription & services revenue (especially USDC revenue), assets under custody, Base transactions and developer activity, and adjusted profitability metrics.

Final thoughts — the larger narrative

It’s easy to get fixated on headline numbers. Q2 showed a clear dip in trading revenue, particularly among retail traders — but the deeper story is far more constructive. Coinbase’s business is diversifying: stablecoins and custody are driving repeatable revenue, Base is building on-chain utility, and subscription products aim to lock-in customers. Yes, one-off issues like the cybersecurity breach hurt the quarter’s operating numbers, but they don’t erase the structural shifts already underway.

Regulatory clarity is arguably the single biggest macro-level change. Laws and frameworks that reduce uncertainty make it easier for institutional capital, TradFi firms, and mainstream commerce to integrate crypto. Combine that with growing on-chain utility, and you have the conditions for a healthier, less speculative ecosystem. Markets will still swing — they always will — but the foundations are being laid for more durable growth.

So be patient, pay attention to the core metrics I outlined, and remember that the story here isn’t that retail traders disappeared; it’s that the industry is maturing. Growth will come from more real-world uses of crypto — payments, custody, staking, and composable on-chain products — not just from trading frenzies. I’ll keep watching the numbers, and if you want a practical way to follow this story, track USDC balances, custody flows, Base activity, and Coinbase’s subscription momentum each quarter.

Parting note

Exchanges are the plumbing of crypto. Their financials don’t just tell you about one company — they reflect how people are actually using crypto. Coinbase’s Q2 revealed a market in transition: less speculative noise, more infrastructure and utility. That’s not the flashiest headline, but it’s the kind of outcome that builds a sustainable industry.

Thanks for reading. If you found this useful, bookmark these metrics and revisit them every quarter — they’ll tell you far more about the evolution of crypto than price alone.

{kind=link}