Table of Contents

- Outline

- What bankification means

- Why banks are racing into crypto now

- How banks will control crypto holdings

- The real stakes: custody, control, and financial freedom

- How to stay in control of your crypto

- Trading opportunities and why signals can help

- What banks will (and will not) do

- Final takeaway

- FAQ

Outline

- What bankification means

- Why banks are racing into crypto now

- How banks will control crypto holdings

- The real stakes: custody, control, and financial freedom

- How to stay in control of your crypto

- Trading opportunities and how signals can help

- FAQs

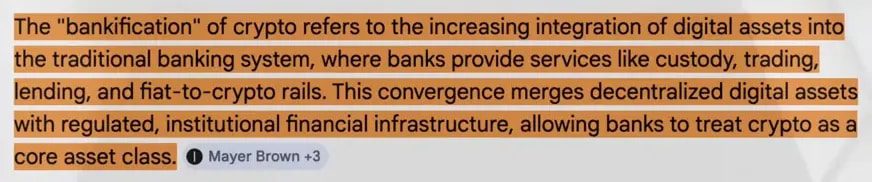

What bankification means

The phrase bankification describes a simple shift: traditional banks are adding crypto trading and custody into the same app where you keep your checking and savings. On the surface it looks like progress—easier onboarding, fewer technical steps, and the familiarity of a regulated institution. But the convenience comes with a tradeoff.

Why banks are racing into crypto now

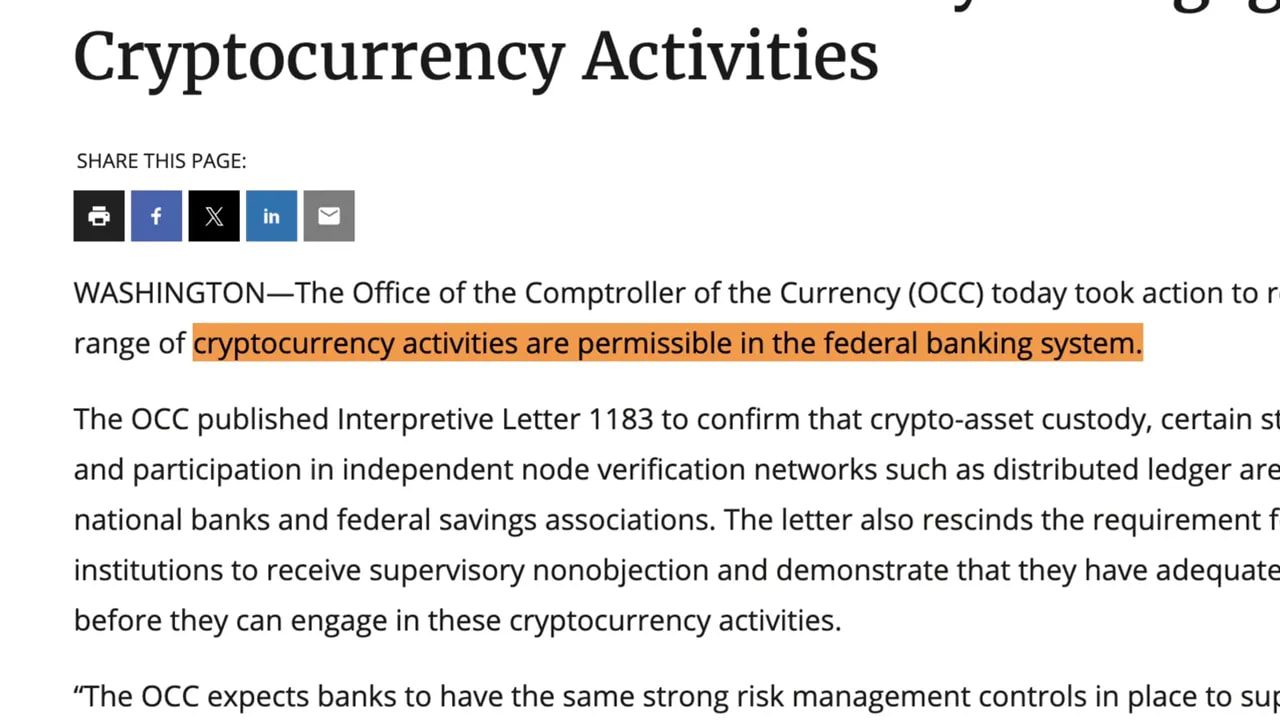

A few forces collided to change the game. Regulators provided clearer guidance that allowed national banks to offer certain crypto services. At the same time, banks watched fintechs and exchanges scoop up profits from trading and yield products. That combination made the move inevitable.

Big names are laying infrastructure now. Some financial firms are building specialized trust banks to serve wealthy clients. Others plan to roll direct crypto access into retail platforms. Third-party integrators are popping up as the plumbing that lets banks plug into blockchains without building everything themselves.

How banks will control crypto holdings

The critical technical detail is custody. When you buy crypto through many bank platforms, you are not given an on-chain address that you control. Instead, banks use an omnibus account. Think of it as one giant box where the bank holds all customer coins and issues internal records that show how much each person “owns.”

On the blockchain, the bank is the owner. For customers, ownership is a digital receipt. That subtle difference matters because the bank can freeze, restrict, or otherwise control access the same way exchanges can. If control is your goal, omnibus custody defeats that purpose.

The real stakes: custody, control, and financial freedom

Cryptocurrency was designed to enable peer to peer value transfer without intermediaries. At the heart of that design are private keys. Whoever controls the keys controls the funds. When banks take custody, they centralize power and recreate many of the failure modes of traditional finance.

This is not just a theoretical risk. Banks have incentives: they want new sources of recurring revenue and ways to protect profit margins that are threatened by decentralized yield and alternate payment rails. If they can capture the onboarding wave of new crypto users, they secure long-term customers and fee streams.

How to stay in control of your crypto

If you value self-sovereignty, the remedy is straightforward: hold your own private keys. That typically means using a self-custodial wallet and storing the keys in a hardware wallet. With self custody nobody can freeze your funds, lock your account, or move your coins without your permission.

Practical steps:

- Learn private key basics — seed phrases, backups, and secure storage.

- Use a hardware wallet for long-term holdings and large amounts.

- Separate accounts — keep day-trading or fiat-conversion funds on regulated platforms, and store long-term holdings in self custody.

- Practice small transfers before moving large sums to new wallets.

Trading opportunities and why signals can help

Mass adoption via banks will increase liquidity and create more trading opportunities across Bitcoin, Ethereum, Solana, and other chains. That creates both more noise and more actionable setups for traders.

For active traders looking to capitalize on fast-moving markets, reliable market analysis matters. Using a trusted source of trade ideas can keep you disciplined and focused. A subtle, useful tool in this environment is high-quality trade signals that highlight potential entries, risk-reward, and asset allocation across chains.

If you plan to split activity between regulated platforms for convenience and your own hardware wallet for custody, consider pairing self custody with a professional approach to trade selection. The right signals service can help you identify opportunities across Bitcoin, Ethereum, and Solana while you maintain control of long-term holdings.

What banks will (and will not) do

Expect banks to position themselves as the simplest, most secure option. They will market convenience, regulation, and protection from scams. They do not need to outlaw self custody to succeed. Changing user preferences and perceptions is enough: if more people trust banks to hold crypto, banks win.

That said, the underlying technology remains permissionless. Self custody cannot be fully erased. The choice users make now—convenience or control—will shape how the ecosystem evolves over the next decade.

Final takeaway

Bank-led crypto access will make buying digital assets easier for millions. That is partly good for liquidity and price discovery. But convenience is not ownership. If avoiding centralized control is important to you, self custody and hardware wallets are essential.

Use regulated platforms when it suits your needs, but keep significant holdings in wallets you control. Trade strategically, and if you rely on active trading for gains, consider using professional-grade signals to spot opportunities across chains while protecting the core of your portfolio with self custody.

FAQ

If I buy crypto through my bank, do I own it?

Not in the same sense as owning on-chain. Most banks use omnibus accounts. You get an internal ledger entry that shows your balance, but the bank holds the on-chain asset. True on-chain ownership requires control of the private keys.

What is an omnibus account?

An omnibus account aggregates many customers’ assets into one on-chain address or custody pool. The institution keeps internal records of who owns what. This simplifies operations but centralizes control.

Can the government ban self-custodial wallets?

A broad ban would be technically and politically difficult. The more realistic risk is regulatory pressure and incentives that make bank custody the path of least resistance for most users. That is why education and self custody matter.

How should I split funds between banks and my own wallet?

Keep short-term capital and fiat-conversion needs on regulated platforms for convenience. Store long-term savings and principle capital in a hardware wallet under your control. Rebalance and move funds when market conditions or personal needs change.

Are crypto trading signals useful with bank-provided trading?

Yes. Bank access will increase liquidity and trading opportunities, but it will also generate more noise. High-quality signals can help you filter setups and manage risk across Bitcoin, Ethereum, Solana, and other chains while you decide where custody should sit.

{kind=link}