Cryptocurrency has revolutionized the way we think about money, offering freedom, innovation, and for some, a chance at life-changing wealth. But not everything that glitters in the crypto world is Bitcoin. Behind the promise of digital gold lurk some of the most dramatic and costly scams ever seen. In this article, we’ll explore the biggest crypto scams in history, how they operated, and what lessons investors can learn to avoid falling victim to similar schemes.

Table of Contents

- Introduction to Crypto Scams

- 1. The Collapse of FTX and Alameda Research

- 2. QuadrigaCX: Canada’s Crypto Tragedy

- 3. Thodex: Turkey’s $2 Billion Crypto Vanishing Act

- 4. Hyperfund: The Pyramid Promise of Big Returns

- 5. HashFlare: Mining Promises That Never Mined

- Conclusion: Lessons from the Biggest Crypto Scams in History

- Frequently Asked Questions (FAQ)

Introduction to Crypto Scams

The crypto space is filled with opportunities, but it’s also a playground for fraudsters. From Ponzi schemes to outright theft, these scams have devastated millions of investors worldwide. Understanding how these scams work is crucial for anyone navigating the crypto market.

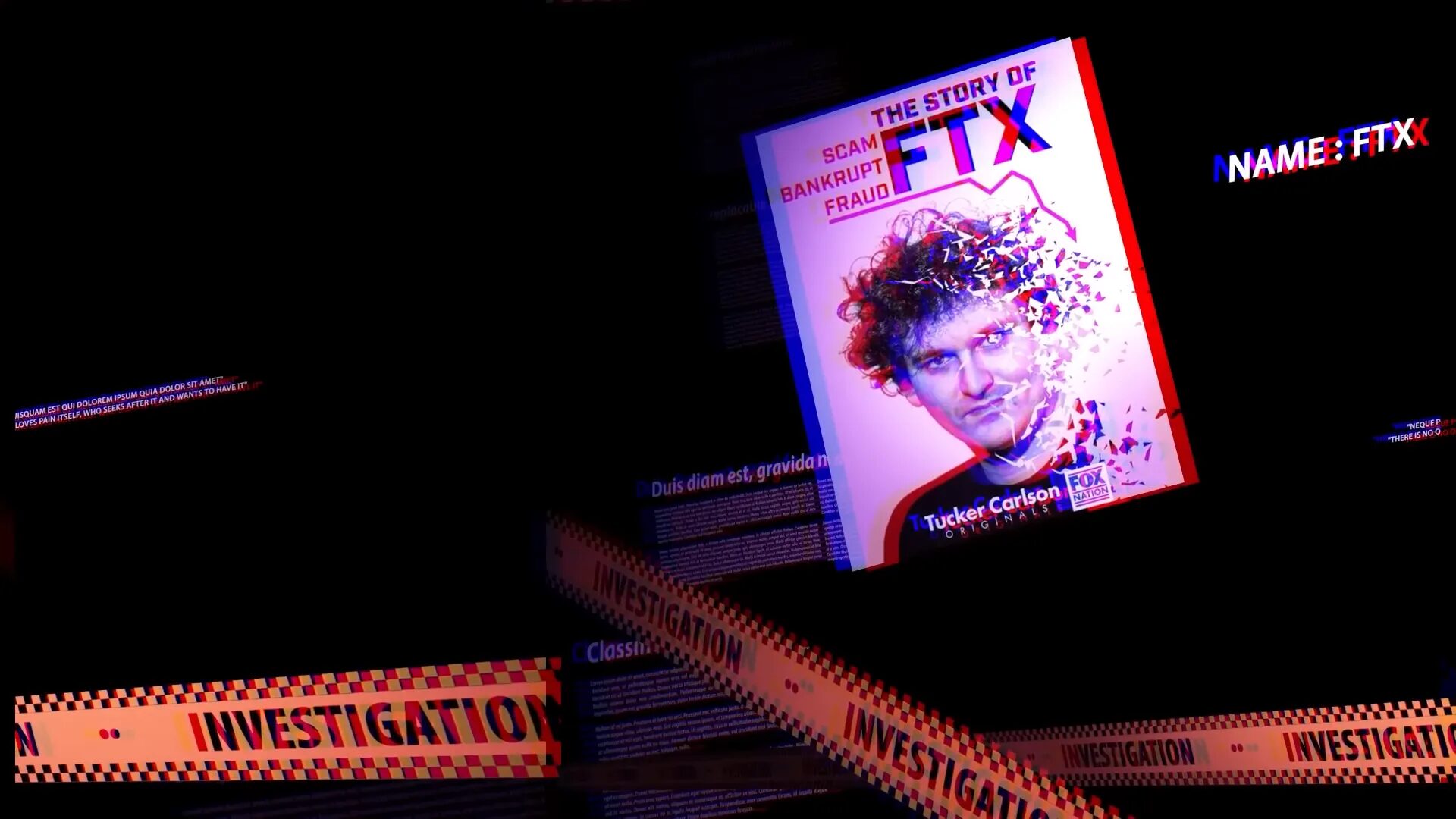

1. The Collapse of FTX and Alameda Research

One of the most shocking crypto scandals in recent memory is the collapse of FTX and its affiliated trading firm, Alameda Research. Founded just three years before its peak valuation, FTX was once worth a staggering $32 billion in 2022.

So, what went wrong? FTX wasn’t just a crypto exchange; it had deep ties to Alameda Research, both controlled by Sam Bankman-Fried (SBF). Customer funds from FTX were secretly funneled to Alameda, where they were used for risky trades and to cover massive losses.

Another critical issue was FTX’s reliance on its own token, FTT, for financial stability. However, FTT lacked liquidity, meaning it was not easy to sell. When Binance, a competitor holding a large amount of FTT, announced it was selling its tokens, panic ensued. Users rushed to withdraw their funds, but FTX didn’t have enough cash on hand to cover the withdrawals, leading to a total meltdown.

Over one million people lost money, with more than $10 billion vanishing seemingly into thin air. The once-mighty FTX crumbled in just days. SBF and Caroline Ellison, who ran Alameda, were charged with fraud and money laundering, convicted, and are now serving prison sentences. This scandal sent shockwaves through the crypto world, highlighting the dangers of blindly trusting even the biggest names in the industry.

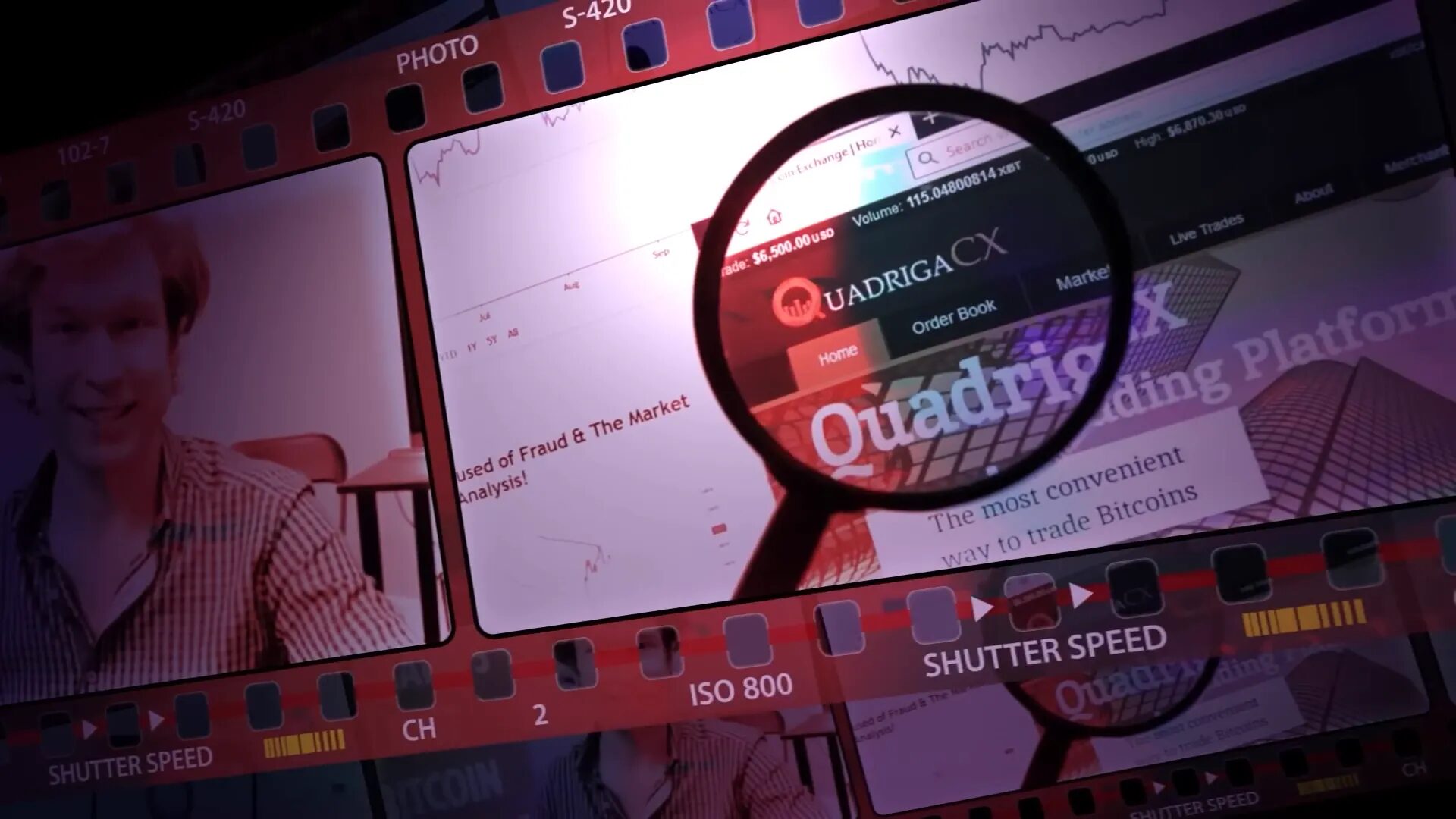

2. QuadrigaCX: Canada’s Crypto Tragedy

QuadrigaCX’s story reads like a thriller. Founded in 2013 by Gerald Cotten and Michael Patryn, it became Canada’s largest crypto exchange with millions of users. However, the situation took a bizarre twist in 2018 when Gerald Cotten died unexpectedly in India due to complications from Crohn’s disease.

Cotten was the only person with access to the private keys for the exchange’s cold wallets, where customer funds were stored. His death seemingly locked away about $200 million of customer funds forever. But investigations revealed a darker truth: the wallets were mostly empty even before Cotten died. Customer funds had been misused for personal expenses and risky trades, and QuadrigaCX was running a Ponzi scheme — using money from new customers to pay off older ones.

The case inspired numerous conspiracy theories, including suspicions that Cotten faked his own death to escape with the money. The scandal gained so much attention that Netflix produced a documentary titled Trust No One: The Hunt for the Crypto King, which is a recommended watch for anyone interested in crypto’s darker side.

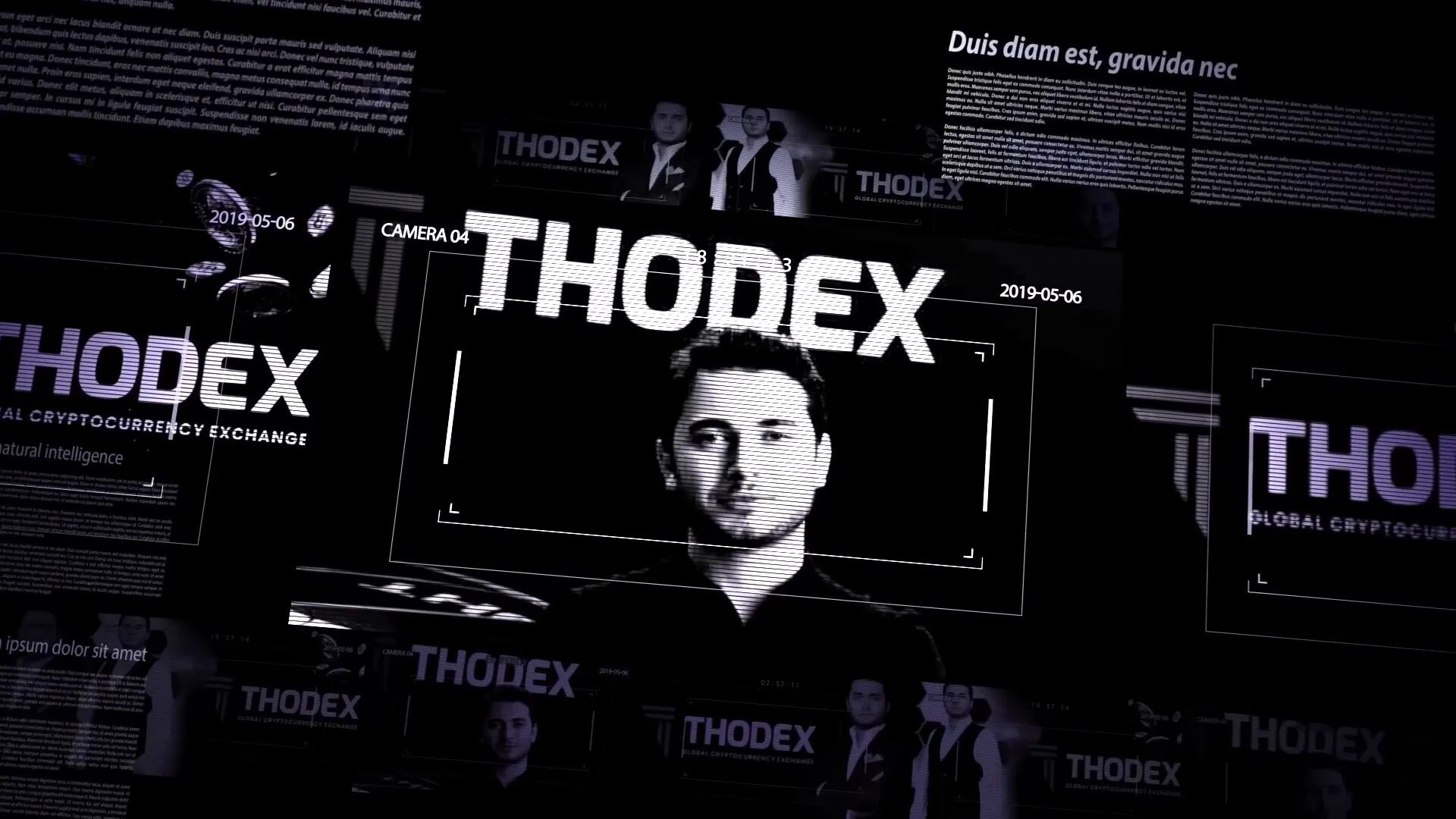

3. Thodex: Turkey’s $2 Billion Crypto Vanishing Act

Thodex was one of Turkey’s largest crypto exchanges, founded in 2017 by Faruk Fatih Özer. It served around 400,000 users across 120 countries, with customers making over 177 transactions per user each month at its peak.

In April 2021, users suddenly found themselves unable to withdraw funds. Thodex claimed it was a temporary glitch, but shortly after, Özer shut down the exchange and disappeared, taking an estimated $2 billion in customer funds with him. Some reports suggest losses could be as high as $2.6 billion.

Investigations uncovered that Thodex was operating a Ponzi scheme. New user deposits were used to pay older users, all while running extravagant promotions to lure more investors. One such campaign gave away millions of Dogecoin, creating buzz and attracting more victims.

Özer was arrested in 2022 and sentenced in 2023 to an unprecedented prison term of 11,196 years. While he claimed innocence, the court was unconvinced. This scandal not only shook the crypto community but also led to stricter regulations in Turkey — a silver lining for future investors.

4. Hyperfund: The Pyramid Promise of Big Returns

Hyperfund, also known by several other names such as Hypercapital and Hyperverse, promised investors huge profits through crypto mining, claiming to pay daily returns ranging from 0.5% to 1%. Founded in 2020, it enticed users with the possibility of doubling or even tripling their investments.

Unfortunately, it was too good to be true. In March 2021, the UK’s Financial Conduct Authority (FCA) issued a warning that Hyperfund was not authorized to offer financial services. By 2022, users faced withdrawal difficulties, a hallmark of Ponzi schemes.

The founder, Sam Li, and top promoter Brenda Chang’e (aka Bitcoin Beauty) were held responsible. Chang’e reportedly earned $3 million promoting Hyperfund at meetings and recruiting more investors. In 2024, the US Securities and Exchange Commission (SEC) charged both with running a pyramid scheme. The case is ongoing, but losses are estimated at $1.89 billion, with more charges expected.

This case underscores a vital rule in crypto investing: if the returns sound unbelievable, they probably are.

5. HashFlare: Mining Promises That Never Mined

HashFlare began in 2015, offering users the chance to lease mining equipment and earn rewards from the cryptocurrency mined. Founded by Sergey Potapenko and Ivan Turogi, the company attracted many with promises of high returns.

However, these promises were empty. HashFlare operated a classic Ponzi scheme, using money from new investors to pay earlier ones. The founders also ran a related scam called Polybius Bank, funneling investor funds into luxury cars, real estate, and personal expenses.

In 2022, the US Department of Justice intervened. By November 2024, both founders were convicted and sentenced to 20 years in prison. Investors lost an estimated $575 million in this scam.

Conclusion: Lessons from the Biggest Crypto Scams in History

Cryptocurrency offers incredible opportunities, but as these stories show, it also comes with serious risks. The scams of FTX, QuadrigaCX, Thodex, Hyperfund, and HashFlare highlight the importance of doing your own research and staying vigilant.

Here are some key takeaways to protect yourself:

- Research thoroughly: Understand the project, founders, and business model before investing.

- Beware of promises of huge returns: If it sounds too good to be true, it probably is.

- Check liquidity and transparency: Avoid projects overly reliant on their own tokens or lacking clear financials.

- Use reputable exchanges and wallets: Prefer platforms with strong security and regulatory oversight.

- Stay informed: Follow trusted sources and keep up with crypto news and regulatory changes.

Remember, there are people out there looking to take your money, so always use your head rather than your heart when investing in crypto.

Frequently Asked Questions (FAQ)

Q1: What are the biggest crypto scams in history?

The biggest crypto scams include the collapse of FTX and Alameda Research, QuadrigaCX, Thodex, Hyperfund, and HashFlare. These scams involved fraudulent use of customer funds, Ponzi schemes, and deceptive practices that led to billions in losses.

Q2: How did FTX collapse affect the crypto market?

FTX’s collapse erased over $10 billion, affecting more than a million users. It shook investor confidence worldwide and highlighted the risks of centralized exchanges mismanaging funds.

Q3: What warning signs indicate a potential crypto scam?

Warning signs include promises of guaranteed high returns, lack of transparency, difficulty withdrawing funds, reliance on new investor money to pay returns (Ponzi schemes), and unregulated platforms.

Q4: How can I protect myself from crypto scams?

Protect yourself by conducting thorough research, using reputable exchanges, avoiding deals that sound too good to be true, and staying updated with crypto regulations and news.

Q5: Are crypto scams decreasing with new regulations?

While regulations are increasing in many countries, scams still persist. Staying informed and cautious remains essential to avoid falling victim.

{kind=link}