Donald Trump’s net worth has reportedly surged from about $2.3 billion before reelection to more than $6 billion roughly 16 months later. That is not normal portfolio appreciation. It is a dramatic repricing of one political family’s fortunes, and a huge chunk of it appears to come from crypto.

The headline number matters, but the structure matters more. This is not just about a president owning Bitcoin or backing friendlier regulation. The core issue is that the same family benefiting from token launches, stablecoin exposure, DeFi revenue, and mining equity also sits next to the machinery that shapes enforcement, legislation, and market legitimacy.

That is what turns a flashy wealth story into one of the most important crypto governance stories in America right now.

Table of Contents

- The scale of the crypto windfall

- The structure behind the money: WLFI, the meme coin, and American Bitcoin

- The meme coin math is ugly

- Why the Justin Sun lawsuits matter more than the headlines

- The separate DOJ probe that may not be separate at all

- What prediction markets reveal about information asymmetry

- The Clarity Act is now the real battlefield

- Institutional money is arriving anyway, but the narrative is cracking

- The real risk to crypto is not regulation. It is capture.

- What happens if Democrats take the House?

- Why this matters for anyone holding crypto

- The bottom line

- FAQ

The scale of the crypto windfall

Forbes and other major outlets have pointed to crypto as the single biggest driver of Trump’s recent wealth expansion. Roughly $3 billion of the increase has been tied directly to digital assets and related ventures.

That alone would be remarkable. But it becomes more consequential when you break down where the money is allegedly coming from:

- Unrealized value in WLFI governance tokens estimated around $570 million

- About $240 million in equity linked to the USD1 stablecoin company

- More than $1 billion in realized cash from WLFI token sales, based on Reuters estimates

- Broader family crypto revenue estimated by Bloomberg at approximately $1.4 billion since January 2025

- About $350 million in trading fees from the Trump meme coin within its first 48 hours

Put bluntly, crypto has become one of the fastest wealth creation engines in Trump’s entire business history.

The structure behind the money: WLFI, the meme coin, and American Bitcoin

The architecture here is intentionally layered, which makes it easy for casual coverage to miss the point.

At the center is World Liberty Financial, or WLFI, a DeFi lending and stablecoin protocol launched in late 2024. The controlling entity is reportedly DT Max DeFi LLC, owned about 70% by Donald Trump and 30% by immediate family members. Under the bylaws, 75% of net protocol revenues and token sale proceeds allegedly flow back to that single LLC.

That means this is not some vague “family-adjacent” project. If the reported structure is accurate, the economics route directly back to a Trump-controlled vehicle.

Alongside WLFI sits the Trump meme coin, issued through two Trump-linked entities, Fight Fight Fight LLC and CIC Digital LLC. Then there is American Bitcoin Corp, the mining business Eric Trump took public via a reverse merger with Hut 8 in September 2025.

These are three separate lanes of crypto monetization:

- DeFi and stablecoins through WLFI

- speculative retail frenzy through the meme coin

- public market mining exposure through American Bitcoin Corp

Together, they create a full-stack crypto empire spanning issuance, fees, treasury-like assets, and public equity narrative.

If you want a broader primer on the mechanics of dollar-pegged crypto assets, this explainer on what stablecoins are and how they work is useful context for understanding why the USD1 angle matters so much politically and financially.

The meme coin math is ugly

The Trump meme coin generated eye-popping early revenue, but the wealth transfer profile is what raises eyebrows.

Blockchain analytics cited in the reporting identified around 45 insider wallets that collectively profited more than $1.2 billion. Meanwhile, over 2 million retail wallets were estimated to be sitting on cumulative losses of roughly $4.3 billion.

That alone sounds like a classic speculative token blow-off. Crypto has seen plenty of those. But this one is different for one reason: the issuer is not just a celebrity or influencer. The issuer is tied to the executive branch.

That means the same ecosystem benefiting from token demand also sits unusually close to decisions involving the SEC, CFTC, Treasury, and broader policy direction. In ordinary markets, speculative excess is one problem. When power and profit are fused together, the risk profile changes completely.

Why the Justin Sun lawsuits matter more than the headlines

The most explosive legal development is not the meme coin. It is the fight between WLFI and Justin Sun.

Sun, the founder of Tron, reportedly invested about $75 million across WLFI tokens and advisory positions beginning in November 2024. Then, in March 2026, the SEC moved to settle its long-running fraud and market manipulation case against Sun and the Tron Foundation.

The settlement terms, as described, were striking:

- A $10 million penalty paid by Rainberry Inc.

- Charges against Justin Sun personally dismissed with prejudice

- No admission of wrongdoing

The timing is what triggered the obvious questions. A major outside buyer of the president’s family token sees his SEC case effectively evaporate after becoming financially intertwined with that ecosystem. Maybe that is coincidence. Maybe it is not. Either way, it is now part of the legal and political backdrop surrounding WLFI.

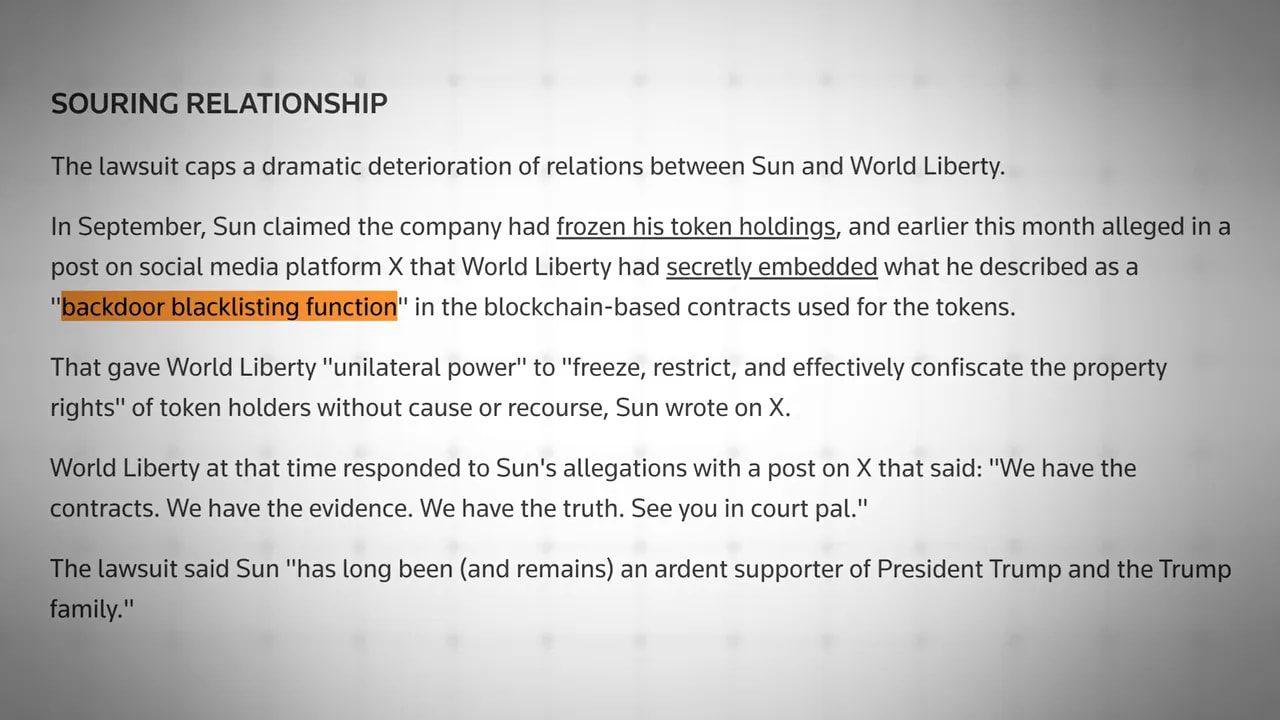

Then the conflict escalated.

On April 22, Sun sued in federal court in Northern California, alleging WLFI had installed a backdoor blacklisting function to freeze roughly $4 billion in his tokens after he refused to invest another $200 million into the USD1 stablecoin. He publicly described WLFI as a “personal ATM” for the Trump family.

WLFI responded on May 4 with a countersuit in Miami-Dade County, alleging defamation, improper token transfers, straw purchases, and a coordinated short-selling campaign.

Here is the key distinction:

- The Florida case is easier for WLFI to manage because it centers on defamation and related claims

- The California case is the real threat because federal discovery could expose internal communications around protocol control, blacklisting tools, and possibly even discussions touching SEC settlement timing

That is why this case matters. Not because crypto loves courtroom drama, but because federal discovery can force sunlight into places press releases never reach.

The separate DOJ probe that may not be separate at all

There is another thread in this story that has received less attention but could prove just as serious: suspiciously timed oil futures trades.

The Department of Justice and the CFTC are reportedly investigating a series of bearish oil trades placed on CME and ICE around major geopolitical communications in March and April 2026.

The timeline is eyebrow-raising:

- $500 million short about 15 minutes before a Truth Social post on Iran de-escalation on March 23

- $960 million short hours before the April 7 ceasefire announcement

- $760 million short about 20 minutes before Iran’s foreign minister announced the Strait of Hormuz reopening on April 17

- $430 million short 15 minutes before Trump extended the ceasefire on April 21

- $920 million short around 17 minutes before an Axios memorandum of understanding leak on May 6

One of those trades alone reportedly netted roughly $125 million in hours. Reuters extended the broader pattern as high as $7 billion across all identified instances.

Investigators are using CME’s Tag 50 trade ID system to trace the accounts. That is the kind of forensic trail that can either collapse a theory quickly or confirm a deeply uncomfortable one.

The awkward wrinkle is that the CFTC, one of the agencies involved, has reportedly seen its workforce cut by about 24% since Trump returned to office. Smaller watchdog, bigger questions.

What prediction markets reveal about information asymmetry

One reason this oil-trade story matters to crypto is that prosecutors are already testing a theory of insider trading in adjacent digital markets.

In April, the DOJ indicted Army Master Sergeant Gannon Van Dyke for allegedly using classified information about the capture of Nicolás Maduro to place winning bets on Polymarket. The result was a jump from about $33,000 to $400,000.

That case applies a misappropriation theory of insider trading to a prediction market. It may sound niche, but the broader principle is not niche at all: if privileged information can lawfully or unlawfully reach a market before the public, those with early access can extract massive value.

The Wall Street Journal also reported that 0.1% of Polymarket accounts captured 67% of all profits. At the same time, the Trump family has exposure to this ecosystem through Donald Trump Jr.’s 1789 Capital and advisory links to Kalshi.

That creates a larger structural question. If a 15-minute lead on a geopolitical post can be worth hundreds of millions in oil futures, what is that information edge worth in Bitcoin options, altcoin derivatives, or event-driven crypto trades?

For active traders, this is where risk management becomes more important than hype. Political headlines now move digital assets almost instantly, and edge can disappear before the broader market catches up. If you use cryptocurrency trading signals, this is exactly the kind of environment where disciplined entries, exits, and position sizing matter more than ever. The market is not just volatile. It is increasingly policy-sensitive.

For anyone comparing research-driven alert services, this guide to the best crypto signals gives a useful overview of what separates quality analysis from noise.

The Clarity Act is now the real battlefield

All of this spills directly into legislation.

The Digital Asset Market Clarity Act passed the House 294 to 134 in July 2025 and is now in Senate Banking Committee markup, with the White House reportedly wanting it signed by July 4.

Under normal circumstances, this would be a major milestone for the industry. Market structure legislation could define the roles of the SEC and CFTC, shape how digital commodities are treated, and give institutions more confidence to allocate capital.

But there is now a giant political obstacle sitting in the middle of it: ethics provisions.

At Consensus Miami on May 6, Senator Kirsten Gillibrand publicly said there would be no votes for the bill without an ethics provision. The proposed rule would bar sitting elected officials and their immediate families from launching, holding, or profiting from token issuances during their term.

That would go straight at the WLFI and Trump token setup as currently described.

The White House position, articulated through digital assets adviser Patrick Witt, is that ethics rules are acceptable if applied “uniformly” and not targeted at specific individuals or offices. In practice, critics hear that as: ethics are fine, as long as they do not actually constrain the arrangement that triggered the ethics concern.

This is why prediction markets on the bill have softened. Odds for Clarity passing in 2026 reportedly fell from around 90% to roughly 60%, with the ethics fight now cited as one of the biggest blockers.

If Clarity fails here, the implications are serious:

- Stablecoin implementation gets delayed

- Market structure reform gets pushed further out

- Institutional integration slows

- The whole legislative agenda may roll into the next presidential cycle

That is not just a Washington process story. It affects token classifications, exchange compliance, product launches, and how aggressively large asset managers continue entering the sector.

If you want more background on why stablecoins have become the center of policy and institutional strategy, this piece on the stablecoin revolution helps frame why lawmakers are fighting so hard over these rules.

Institutional money is arriving anyway, but the narrative is cracking

One of the strangest parts of this whole saga is that institutional adoption has continued despite the political overhang.

Examples cited include:

- Vanguard reversing its crypto ban in December 2025

- Morgan Stanley launching MSBT and gathering $200 million in AUM within three weeks

- BlackRock’s IBIT pulling in about $721 million over three trading days, bringing assets under management to roughly $66.7 billion

So capital is still flowing in. But that does not mean the market is healthy in a structural sense.

The bullish institutional narrative has depended on one central idea: crypto is maturing into a legitimate asset class governed by neutral rules. If the public starts to believe instead that the rules are being written around one politically connected family’s financial interests, that legitimacy premium starts to erode.

And once legitimacy is damaged, the cost is not limited to one token or one protocol. It touches the entire asset class.

The real risk to crypto is not regulation. It is capture.

This is the point many people still miss.

The biggest threat here is not anti-crypto hostility from regulators. It is the perception, and possibly the reality, of regulatory capture. In other words, crypto policy being shaped by actors who are financially entangled with the very structures they are supposed to regulate or stand apart from.

That kind of risk is harder for markets to price than a straightforward crackdown.

A hostile regulator can at least be modeled. Capture is murkier. It changes incentives, delays accountability, politicizes enforcement, and makes legal outcomes feel selective. Markets hate uncertainty, and selective enforcement is uncertainty with a political badge on it.

That is also why self-custody and decentralized risk management become more compelling in this environment. If the rules become partisan footballs, then relying entirely on centralized intermediaries or policy assumptions becomes a much more fragile strategy.

For traders navigating these swings, the goal should not be chasing every headline candle. It should be staying systematic. Used properly, cryptocurrency trading signals can help filter emotionally charged market moves into clearer setups, especially when legislative developments and political litigation start moving sectors unevenly across Bitcoin, altcoins, and DeFi tokens.

What happens if Democrats take the House?

One more forward-looking piece matters here.

If Democrats win the House in 2026, the first major crypto-related legislative push may not be a crackdown on the industry itself. It may be retroactive ethics enforcement targeting the kinds of political token arrangements that define this cycle.

That would be a very different kind of shock.

Not “crypto is banned.”

More like: specific structures, issuances, or conflicts are criminalized or aggressively pursued after the fact. That changes the risk calculus for a lot of assets currently benefitting from the perception that they sit under the “digital commodity” umbrella.

In other words, the market may be underestimating how much current valuations rely on a political status quo that could shift abruptly.

Why this matters for anyone holding crypto

Strip away the personalities and the partisan noise, and the practical implications are pretty straightforward.

- Position sizing matters more when policy risk is concentrated around one family’s legal exposure

- Headline risk is now legislative risk, not just macro or exchange risk

- Self-custody arguments are stronger when regulatory frameworks become politicized

- Token-specific due diligence matters because some projects may be repriced if ethics rules tighten

- Market structure reform is no longer a clean bullish catalyst because it may be delayed or reshaped by scandal

The market can handle clear rules. What it struggles with is a rulebook that seems to bend around insiders while everyone else is told to wait for clarity.

The bottom line

Trump’s wealth appears to have nearly tripled, and crypto looks to be one of the main reasons why. The family’s reported exposure spans DeFi, stablecoins, meme coins, and mining. At the same time, WLFI is in a legal war with Justin Sun, the DOJ and CFTC are digging into suspiciously timed oil futures trades, and the most important crypto bill in the US is now bottlenecked by ethics provisions aimed squarely at political token profiteering.

That is not a side story. It is the story.

The future of US crypto regulation may now hinge on a brutally simple question: can lawmakers write rules that constrain the exact arrangement currently enriching one of the most powerful families in American politics?

If the answer is yes, the industry may finally get durable structure, though probably with sharper ethics guardrails than some in crypto hoped for.

If the answer is no, the cost could be much larger than one scandal. It could delay comprehensive legislation, fracture the legitimacy narrative, and drag the whole market into a much uglier political fight through the 2026 midterms and beyond.

FAQ

How did Trump reportedly make so much money from crypto?

The reported gains come from multiple crypto-linked ventures, especially WLFI governance tokens, USD1 stablecoin exposure, token sale proceeds, fees from the Trump meme coin, and related family-controlled entities. Estimates suggest crypto accounts for about $3 billion of the recent jump in net worth.

What is WLFI?

World Liberty Financial, or WLFI, is a DeFi lending and stablecoin protocol launched in late 2024. It is reportedly controlled through DT Max DeFi LLC, with most economic benefits flowing back to a Trump family-owned structure.

Why is the Justin Sun case such a big deal?

Because the California lawsuit could open federal discovery into WLFI’s internal operations, including blacklist functionality, operational control, and potentially communications relevant to regulatory decisions. That makes it far more dangerous than a standard public dispute.

What does the oil futures investigation have to do with crypto?

The core issue is information asymmetry. If traders had advance knowledge of market-moving political communications in oil, the same logic applies to crypto markets, where prices react instantly to geopolitical and regulatory signals.

What is the Clarity Act and why does it matter?

The Digital Asset Market Clarity Act is a major US crypto market structure bill. It could define regulatory roles and provide long-awaited rules for digital assets. Right now, ethics provisions tied to political token ownership are one of the biggest threats to its passage.

Could ethics rules hurt the broader crypto market?

Short term, yes, because they could delay legislation and unsettle investor expectations. Long term, strong ethics rules could help the market by restoring credibility and reducing the perception that crypto policy is being shaped for private political gain.

How should traders respond to this kind of political market risk?

Focus on risk management, not headline chasing. Smaller position sizes, stricter entries and exits, and disciplined strategy matter more when legislation, lawsuits, and political influence can move markets as much as fundamentals. That is also why some traders rely on structured cryptocurrency trading signals to stay systematic during high-volatility periods.

{kind=link}