Donald Trump’s ban on a retail central bank digital currency was hailed as a major victory for privacy, sovereignty, and the anti-surveillance wing of the crypto world. On paper, it looked like Washington had slammed the door on a digital dollar.

In reality, it may have done something far more significant.

Rather than creating a Federal Reserve-issued digital currency directly, the United States has moved toward a model built on privately issued stablecoins, supervised by the Treasury and backed almost entirely by short-duration US government debt. The legal vehicle for that shift is the GENIUS Act, and it may end up functioning as the de facto digital dollar system for the United States.

That matters for three reasons.

-

It creates a new, structurally growing source of demand for US Treasuries.

-

It gives stablecoin issuers the yield on reserves while ordinary users get none of it.

-

It embeds freezing, blocking, and transaction surveillance directly into the architecture of digital dollars.

So yes, the CBDC may be banned in name. But the financial rails being built look awfully similar to the thing many people thought they had just defeated.

Table of Contents

- The ban on a CBDC was only half the story

- What the GENIUS Act actually does

- Why stablecoins have become critical to US debt markets

- A modern form of financial repression

- The real cost to stablecoin users

- The privacy problem is not theoretical

- Freezing and blocking are now features, not exceptions

- Wall Street’s sudden conversion to crypto has a motive

- The likely corporate winners

- The tail risk nobody wants to talk about

- So is the CBDC really dead?

- The bottom line

- FAQ

The ban on a CBDC was only half the story

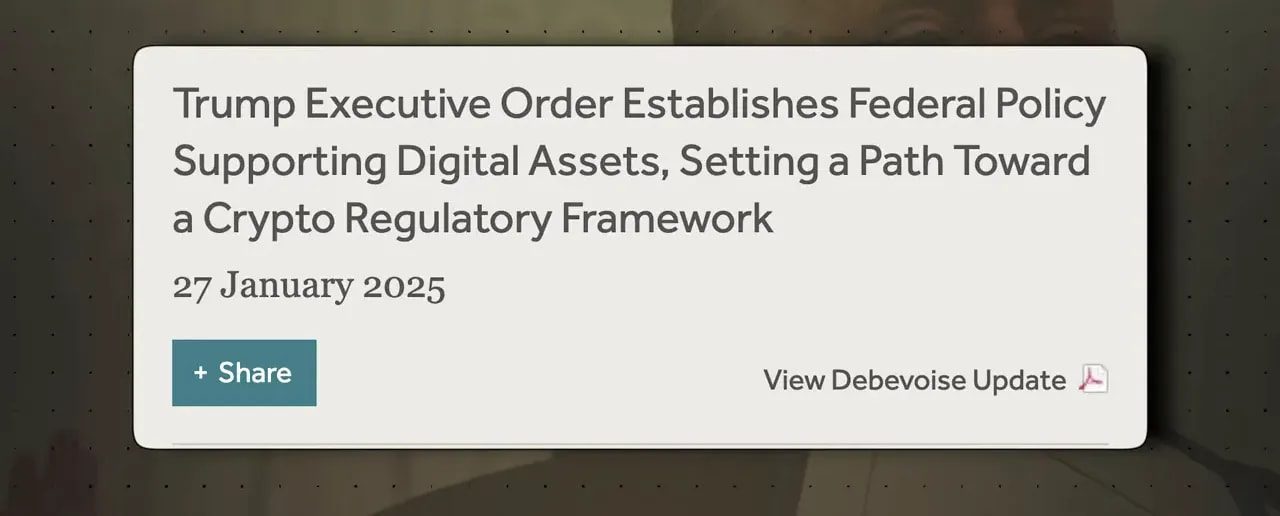

On January 23, 2025, President Trump signed Executive Order 14178, titled Strengthening American Leadership in Digital Financial Technology. The order prohibited federal agencies from establishing, issuing, or promoting a central bank digital currency in the United States.

The justification was exactly what many in crypto had long demanded from policymakers: privacy, sovereignty, and protection from government surveillance.

So far, so good.

But hidden in the same order was another directive that pointed in a very different direction. It explicitly promoted privately issued, dollar-backed stablecoins as the preferred path for digital payments infrastructure.

That was not a contradiction. It was the strategy.

Less than six months later, on July 18, 2025, Trump signed the Guiding and Establishing National Innovation for US Stablecoins Act, better known as the GENIUS Act, into permanent federal law.

That law established the framework for a stablecoin system that is private in branding, but public in strategic purpose.

What the GENIUS Act actually does

The mechanics matter here, because this is where the policy reveals itself.

Under the GENIUS Act:

-

Every dollar of stablecoin supply must be backed one-to-one by short-duration US Treasury bills, cash, or overnight repos backed by Treasuries.

-

Issuers with more than $10 billion in supply must come under direct supervision from the Treasury, the OCC, and the FDIC.

-

Stablecoin issuers are explicitly prohibited from paying interest, yield, or any equivalent return to the end user.

That last point is the one most people are likely to underestimate.

If you hold a regulated stablecoin under this framework, you get the convenience of digital dollars. What you do not get is the income generated by the reserves backing your tokens. The issuer earns that. The Treasury benefits from the demand for its debt. You get a payment tool.

That is not a bug in the design. It is the design.

Why stablecoins have become critical to US debt markets

To understand why Washington is leaning into this model so aggressively, you have to zoom out from crypto and look at the bond market.

The United States needs reliable buyers for its debt. Historically, foreign governments and overseas investors played a major role in absorbing Treasuries. That support base is no longer as dependable as it once was.

Foreign holdings of American Treasuries have been shrinking. Chinese holdings fell to $682 billion by November 2025, the lowest level since 2008 and nearly 47% below the 2013 peak. Foreign investors as a group now hold just 32.4% of outstanding US Treasuries, the smallest share since 1997. At the same time, global central banks have been piling into gold, with official reserves crossing $5 trillion in early 2026.

That leaves Washington with a problem: who will buy the mountain of short-term government debt that needs refinancing?

The answer, increasingly, is stablecoin issuers.

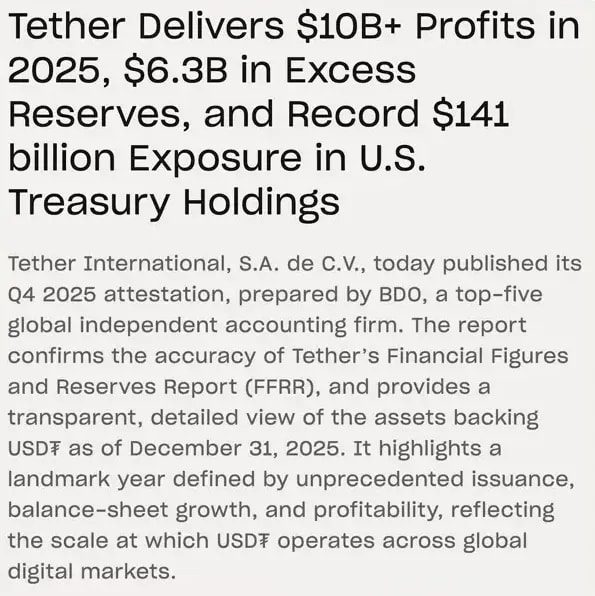

Tether’s reported exposure to US Treasury instruments reached $141 billion by the end of 2025, with direct holdings above $122 billion. Circle’s reserve fund disclosed roughly $68.167 billion in assets as of March 20. Combined, those two issuers alone control around $200 billion in short-duration sovereign debt.

That is not a niche corner of the market anymore. That is strategic scale.

And Treasury Secretary Scott Bessent has been unusually open about the intent. He stated publicly that stablecoins could draw in new sources of funding for the US. He also projected that the stablecoin market could grow into a multi-trillion dollar industry, absorbing as much as $2 trillion of incremental Treasury demand by the end of the decade.

So if you were wondering whether stablecoins are merely a side effect of financial innovation, the answer is no. Stablecoins are now policy.

A modern form of financial repression

The easiest way to think about this system is as a 21st-century version of financial repression.

During and after World War II, the US government kept Treasury yields artificially low so it could finance massive debts while inflation quietly eroded the real value of savings. The tools were different then. Today, the mechanism is subtler.

No one needs to impose direct capital controls or hard interest-rate ceilings. Instead, the state can encourage or regulate a system in which millions of people hold digital dollars that are fully backed by Treasuries, while the yield generated by those reserves is captured upstream by issuers and the sovereign itself.

The public provides the funding base. The returns flow elsewhere.

That makes stablecoin growth enormously attractive from a fiscal point of view. It manufactures a captive domestic buyer for short-dated government paper at precisely the moment foreign demand is losing steam.

The real cost to stablecoin users

Now let’s bring this down from macro policy to household math.

Say someone keeps $10,000 in a regulated stablecoin for payments, transfers, or trading. Under the GENIUS Act structure, that holder cannot receive interest on the balance. The issuer can take that reserve base, buy three-month Treasury bills yielding around 3.7%, and earn roughly $370 per year on those funds.

The user gets utility. The issuer gets the spread.

Tether reportedly generated more than $10 billion in net profit across 2025, driven overwhelmingly by this reserve-income model. That is one of the clearest examples of what is happening here. The yield that might have gone to depositors in a more competitive environment is being redirected to a small group of large, regulated players.

For active market participants, this creates an odd split. Stablecoins remain essential trading collateral across exchanges, DeFi platforms, and cross-border transfers, but simply holding them idle becomes increasingly expensive in opportunity-cost terms. That is one reason serious traders tend to focus on capital efficiency and timing. If you are navigating rotations between majors, altcoins, and ecosystem plays, having strong market analysis matters far more when your base collateral itself is non-yielding. That is also where services such as cryptocurrency trading signals can be useful for some traders, especially when trying to minimize dead capital and act on high-conviction setups rather than leaving funds parked indefinitely.

The privacy problem is not theoretical

The financial issue is serious enough. But the civil-liberties issue may be even more important.

The infrastructure being built through regulated stablecoins is not just a payment network. It is a programmable, traceable, censorship-enabled substitute for cash.

There is already precedent for how this works in practice.

In August 2022, the Office of Foreign Assets Control sanctioned Tornado Cash, placing open-source software code onto its sanctions list for the first time. Within hours, Circle blacklisted associated addresses and froze assets linked to the protocol, before any court had ruled on the legality of the action.

Later, the Fifth Circuit ruled that OFAC had exceeded its authority because immutable software code is not property. Treasury eventually delisted Tornado Cash in March 2025.

But by then, the key point had already been proven: the system could freeze wallets on command.

The legal debate came afterward. The operational capability came first.

That distinction matters enormously, because once the rails exist, they can be used by whichever administration happens to be in power.

Freezing and blocking are now features, not exceptions

On April 8, 2026, FinCEN and OFAC jointly proposed rules implementing the GENIUS Act’s anti-money laundering provisions. Those rules formally require every permitted payment stablecoin issuer to maintain the technical ability to block, freeze, and reject suspicious transactions.

So this is no longer discretionary compliance. It is a federally mandated design requirement.

The enforcement history is already substantial:

-

Tether disclosed freezing more than 7,200 addresses and about $3.3 billion of supply between 2023 and 2025.

-

Circle froze hundreds of addresses in the same broad period.

-

In March 2026, Circle froze 16 operational business wallets in response to a sealed civil case before later reversing the action after backlash.

Supporters will say these tools target criminals. Critics will say the infrastructure can be expanded, repurposed, or abused. Both statements can be true at once.

The uncomfortable question is not whether these powers will be used. They already are. The real question is how narrowly they remain confined once digital dollars become deeply embedded in everyday finance.

If your money can be frozen, your transactions screened, and your wallet behavior monitored, then whatever else this system is, it is not cash in the traditional sense.

Wall Street’s sudden conversion to crypto has a motive

One of the more entertaining parts of this whole story is watching the old guard perform an ideological U-turn at high speed.

Back in 2017, Jamie Dimon famously called Bitcoin a fraud and said he would fire any JPMorgan trader reckless enough to touch it. Over the years, crypto was dismissed as a pet rock, a criminal tool, and an asset class with no real value.

Then the tone changed.

By late 2025, Dimon was saying that crypto is real, blockchain is real, and stablecoins are real. In his 2026 shareholder letter, he explicitly identified stablecoins, tokenization platforms, and smart contract infrastructure as new competitors to JPMorgan’s core businesses.

That is not a philosophical awakening. It is a business adaptation.

JPMorgan’s blockchain settlement platform, Kinexys, is already processing more than $5 billion per day in institutional flow, with cumulative volume above $3 trillion. Its deposit token, JPMD, is now live on Coinbase’s Base network and being integrated more broadly.

Elsewhere:

-

BlackRock’s tokenized money market fund BUIDL has grown to around $1.7 billion to $2 billion.

-

BNY Mellon is custodying the Circle Reserve Fund, BUIDL, and other digital asset products.

-

Visa launched USDC settlement on Solana and committed as a validator on Circle’s upcoming ARC blockchain.

-

Mastercard acquired stablecoin infrastructure firm BVNK for up to $1.8 billion.

-

PayPal’s PYUSD supply reportedly grew more than 500% during 2025 to around $4 billion.

The rails are being built by the same institutions crypto was supposed to route around. The difference is that now the business model is obvious: every layer of tokenized finance can collect a fee.

For traders, this institutional buildout also changes where opportunity may emerge. As stablecoin infrastructure expands across chains such as Base and Solana, liquidity flows and narrative cycles can become highly chain-specific. That tends to create bursts of relative strength in exchange tokens, infrastructure plays, and ecosystem assets. It is exactly the kind of environment where disciplined execution matters more than hype, and where some market participants lean on cryptocurrency trading signals to track momentum, breakout zones, or sector rotations more systematically.

The likely corporate winners

If the GENIUS Act framework continues to scale, the main equity beneficiaries form a fairly tight cluster.

Circle sits right in the middle of the regulated stablecoin arms race, especially after receiving conditional OCC approval to operate as the first national digital currency bank.

Coinbase benefits from reserve interest on USDC held on-platform and a share of income on off-platform supply.

BNY Mellon and State Street are positioned as custody and infrastructure providers for tokenized money-market products and stablecoin reserves.

Visa, Mastercard, and PayPal each have clear routes into settlement, payments, and merchant infrastructure.

In simple terms, if money becomes tokenized but remains tightly regulated, the likely winners are not cypherpunk idealists. They are banks, custodians, payment giants, and compliant stablecoin issuers.

The tail risk nobody wants to talk about

For all the talk of safety and fully backed reserves, stablecoins still carry systemic risk.

The most important recent example came in March 2023, when Circle revealed that roughly $3.3 billion of USDC reserves were sitting at Silicon Valley Bank when regulators shut it down. USDC fell as low as $0.87. DAI dropped too because of collateral linkage. The peg only recovered because the Federal Reserve, FDIC, and Treasury stepped in under a systemic-risk exception to protect uninsured depositors.

That incident delivered an awkward truth. The stablecoin architecture was rescued by the very sovereign backstop it was supposedly designed to sit apart from.

Now scale that kind of stress event to a reserve base closer to $200 billion and the implications become much less comfortable.

If stablecoins become critical plumbing for the dollar system, then any disruption in issuer reserves, banking access, or redemption confidence stops being a crypto problem. It becomes a national financial-stability problem.

So is the CBDC really dead?

Not in any meaningful functional sense.

What has died, at least for now, is the politically toxic version of a digital dollar where the central bank issues it directly to the public. What has emerged instead is a hybrid model in which private companies issue the tokens, government debt backs them, regulators supervise them, and compliance features are built in from day one.

That arrangement may even be more politically durable than a formal CBDC because it preserves the optics of market competition while achieving many of the same outcomes.

The government gets a new domestic buyer base for Treasuries. Issuers get reserve income. Big banks and payment networks get a profitable seat at the table. Consumers get convenience, but surrender yield and potentially a significant amount of privacy.

That is why the CBDC ban looks less like a full stop and more like one of the most effective pieces of monetary misdirection in years.

The bottom line

The GENIUS Act is not just stablecoin regulation. It is a blueprint for how the United States may digitize the dollar without ever calling it a CBDC.

It solves a Treasury funding problem by channeling stablecoin reserves into government debt. It privatizes reserve income by blocking yield payments to ordinary holders. And it normalizes programmable controls over digital money through legal compliance requirements that include tracing, blocking, and freezing.

Yes, the convenience is real. So are the profits for issuers and institutions.

But so is the cost.

If this framework becomes dominant, then the future of money in America may not be decentralized, neutral, or cash-like at all. It may be tokenized, regulated, surveilled, and rentable.

And that would change everything.

FAQ

What is the GENIUS Act?

The GENIUS Act, short for the Guiding and Establishing National Innovation for US Stablecoins Act, is a US law that creates a federal framework for stablecoin issuers. It requires one-to-one backing with cash, short-duration Treasuries, or repo agreements backed by Treasuries, and places larger issuers under direct federal supervision.

Did Trump ban the digital dollar?

Trump banned a retail central bank digital currency through executive order, but at the same time promoted privately issued dollar-backed stablecoins. In practice, that means a direct Fed-issued CBDC was blocked while a stablecoin-based digital dollar framework was encouraged.

Why are stablecoins important to the US Treasury?

Because regulated stablecoins must hold reserves in short-duration US government debt or equivalent assets. As the stablecoin market grows, issuers become large and steady buyers of Treasuries, helping the government finance and refinance its debt.

Do stablecoin users earn interest under the GENIUS Act model?

No. The framework explicitly prohibits stablecoin issuers from paying interest or yield to token holders. The reserve income goes to the issuer rather than the consumer.

Can regulated stablecoins freeze funds?

Yes. The regulatory model requires issuers to maintain the ability to block, freeze, and reject suspicious transactions. This makes censorship and compliance controls part of the core design of the system.

Who benefits most if this stablecoin framework expands?

The biggest likely beneficiaries are regulated stablecoin issuers, crypto exchanges with revenue-sharing agreements, large custodians, payment networks, and major financial institutions building tokenized settlement infrastructure.

{kind=link}