")

There is a brutally simple idea that has outperformed what most people consider the gold standard of investing.

For the last 56 years, a portfolio made up of just the top 10 US stocks by market cap, rebalanced regularly, has beaten the S&P 500 by a huge margin. Not by a little bit. By more than 3x over time.

That sounds wrong at first.

We are taught that diversification is safety, concentration is danger, and that owning more names somehow automatically means owning less risk. But the data points toward something much more uncomfortable. In market cap weighted markets, concentration is not an accident. It is the engine.

And once you really understand why that works in equities, it becomes very hard to ignore the implications for crypto.

Table of Contents

- Why the S&P 500 is already more concentrated than most people think

- Why concentration works: most stocks are dead weight

- The Mag 7 era is not an anomaly. It is a live example of the rule

- Is concentration risk actually as dangerous as people say?

- Why “buying low” often turns into buying lower

- Now bring that logic into crypto

- Bitcoin dominance looks even more extreme than the stock market

- What the data suggests for crypto portfolio construction

- You do not need to pick the unicorns early

- Where trading signals fit into a market like this

- Why this thesis pushes many people back toward Bitcoin

- Stablecoins, exclusions, and why definitions matter

- The real takeaway

- FAQ

Why the S&P 500 is already more concentrated than most people think

The S&P 500 is often treated like the diversified default. It tracks 500 large US companies and is rebalanced quarterly. If a company falls out of the top ranks, it gets removed and another takes its place.

But there is a detail that matters a lot: it is market cap weighted.

That means the biggest companies dominate the index. When Nvidia, Apple, Microsoft, Amazon, or other giants surge, they have an outsized impact on total returns. Smaller constituents exist in the index, but many barely move the needle.

So although people talk about the S&P 500 as if it is a broad basket of equal opportunities, it is not. It is already a portfolio that leans heavily toward the biggest winners.

That matters because the “simple strategy” is not some obscure quant trick. It is really just this:

- Take the logic of a market cap weighted index

- Lean into it further

- Own the largest companies

- Rebalance as leadership changes

When this was compared across different levels of concentration, something interesting happened.

Owning only the single largest stock was not better than the index. That is too concentrated and too dependent on one throne-holder staying on top. But once you move into a slightly broader basket, such as the top 3, top 5, or especially top 10, the results begin to improve dramatically.

The top 10 delivered roughly 12.68% annualized returns, which compounded into dramatically better long-run performance than the full S&P 500.

Why concentration works: most stocks are dead weight

This is the part that really flips the usual investing narrative upside down.

Research by Hendrik Bessembinder, who studied virtually every US stock since 1926, found something astonishing:

- 54% of stocks lose money over their lifetime

- Only 4% of stocks account for the entire net wealth creation of the market

- Roughly 96% of stocks do not beat Treasury bills

Read that again because it is wild.

The vast majority of publicly traded companies, even in the most developed equity market in the world, do not create meaningful long-term wealth beyond what short-term government debt could have delivered.

And the upside is insanely concentrated. Around 90 stocks created half of all stock market wealth.

That means market returns are not produced by “the average stock.” They are produced by a tiny minority of monster winners.

Think Amazon. Apple. Nvidia.

The winners do an absurd amount of the heavy lifting.

The Mag 7 era is not an anomaly. It is a live example of the rule

If this sounds abstract, recent market history makes it very concrete.

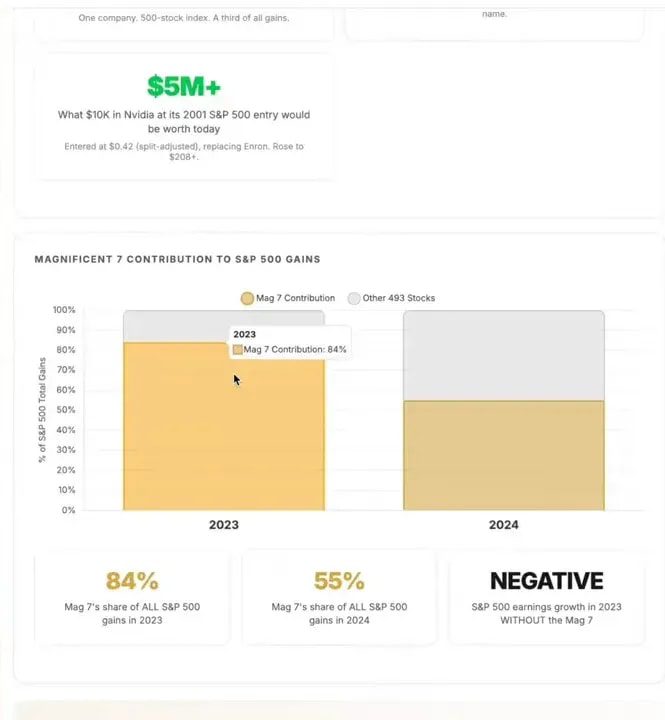

In 2023, about 84% of the S&P 500’s gains came from the Magnificent Seven. In 2024, that figure was still around 55%. Without those names, the broad index would have looked dramatically worse, and in 2023 it would have been negative.

At one point in 2024, roughly a third of the S&P 500’s return was attributable to Nvidia alone. In 2020, Apple had a similarly outsized role.

This is not some weird distortion of the market. This is how markets often work. A handful of dominant businesses capture the economics, capture investor attention, and capture most of the gains.

That creates discomfort because it feels risky. But the discomfort is more psychological than statistical.

Is concentration risk actually as dangerous as people say?

People panic when they hear that a few names make up a large chunk of an index. The instinct is understandable. If a small group of companies is driving returns, surely that must mean danger is building.

Except global market history does not strongly support that conclusion.

Across stock markets around the world, concentration is normal. On average, the top 10 companies in a country make up around 48% of that market. The US has been around 40%, which is high by its own historical standards but still not especially outrageous compared with other countries.

There are even more extreme examples. Finland once saw Nokia make up roughly 70% of the entire stock market.

That does not mean concentration can never become a problem. It can. But the broader research suggests that high concentration has had a statistically insignificant relationship with future returns. In plain English, a concentrated market does not automatically predict weak performance ahead.

That clashes with the deeply ingrained “buy low, sell high” mindset. We want to believe that expensive winners must be near the end and beaten-down laggards must be bargains.

But often the real lesson is much less romantic: buy high, sell higher.

The winners tend to keep winning.

Why “buying low” often turns into buying lower

This may be the most useful part of the whole framework.

People love bottom-fishing. A chart that is down 80% feels cheap. A former market darling that has been bleeding for two years feels like an opportunity. But price alone does not create value.

Something that has gone down a lot can still go down more. In fact, markets are full of assets that never reclaim their former highs.

Meanwhile, the big winners often look expensive the entire way up. They make new highs, get called overvalued, then go on to make even more highs.

There is similar evidence in equities showing that buying the S&P 500 at all-time highs has often produced better results than waiting around for the perfect pullback. Why? Because over long stretches, the index trends upward. If you keep waiting for a better price, the market often leaves you behind.

It is not a comfortable truth, but it is one markets keep repeating.

Now bring that logic into crypto

This is where things get really interesting.

If only 4% of stocks drive essentially all long-term stock market wealth, what should we expect in crypto, a market made up largely of early-stage, high-risk projects?

Crypto tokens are not identical to stocks, obviously. Some behave more like commodities, some are utility assets, some have governance features, and some are tied to entirely different token economics. But in spirit, a huge portion of the market can be thought of as tech startups financed through tokens rather than equity.

And that should immediately raise your eyebrows, because startups already have brutal failure rates. Tech startups in emerging sectors have even worse odds. Crypto combines both.

If startup failure rates are commonly above 90%, and more than 60% of tokens ever listed on CoinGecko are already considered dead, then the expectation that you will casually pluck the next unicorn from the graveyard is, frankly, not a serious strategy.

Picking stocks is hard. Picking the future winners in a chaotic, ultra-early, reflexive market like crypto is harder.

This is also why it helps to compare crypto and equities with a bit of sobriety rather than hype. If you want a broader framework for thinking through that balance, this breakdown of stocks vs crypto is a useful companion read.

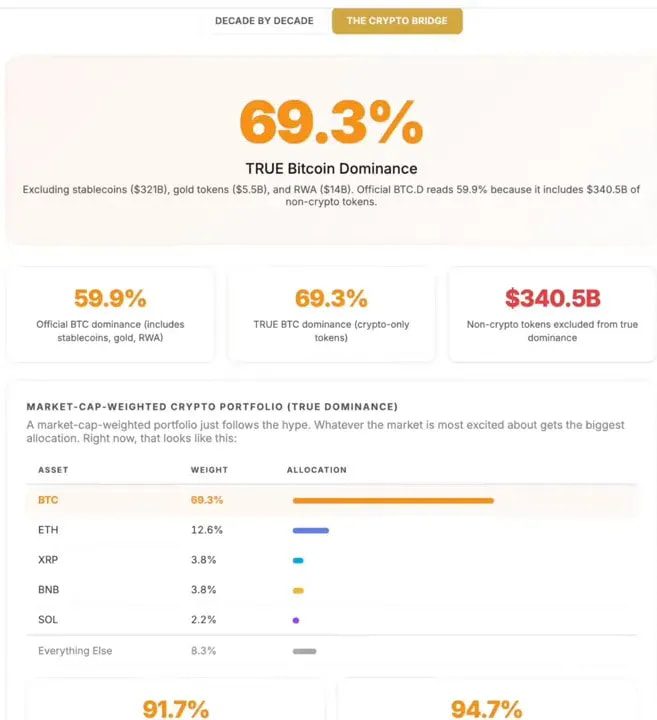

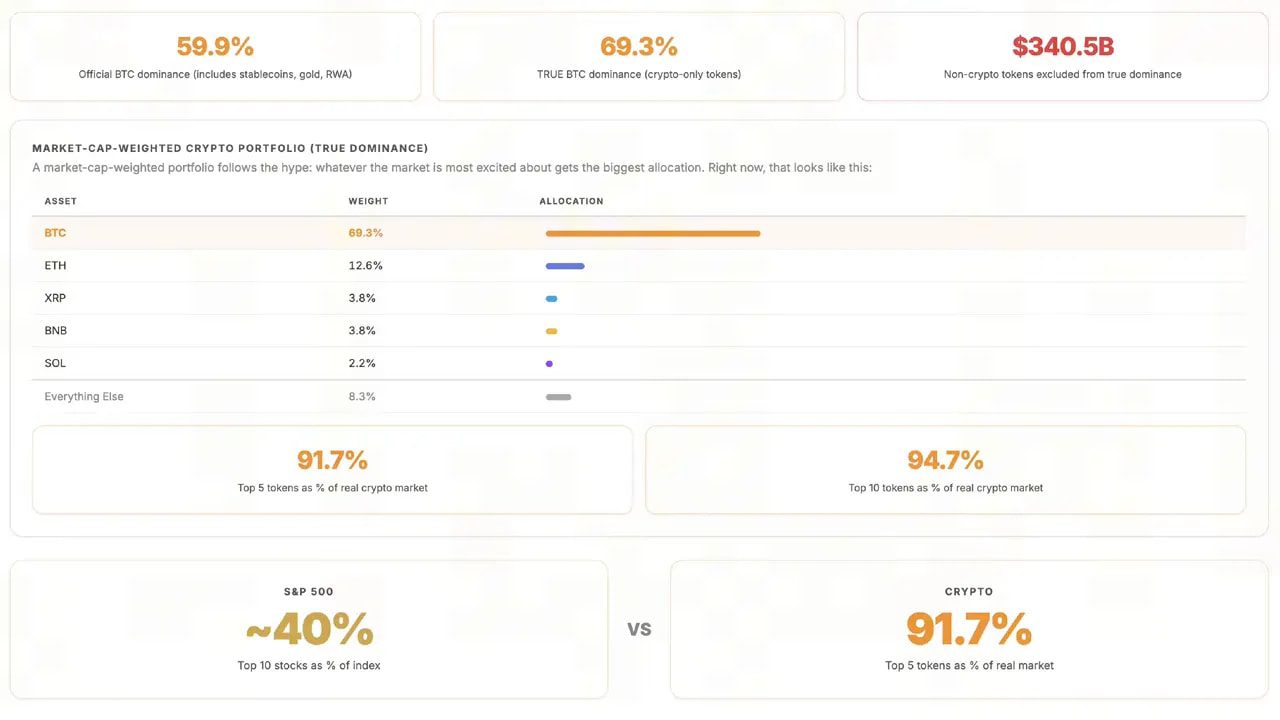

Bitcoin dominance looks even more extreme than the stock market

Once non-token categories such as stablecoins and other assets are stripped out, the crypto market becomes even more top-heavy than many people realize.

By that framing:

- Bitcoin accounts for roughly 70% of the market

- Ethereum is around 12.5%

- XRP is roughly 4%

- Everything else in the top 10 makes up the remaining slice

That means around 95% of crypto’s value sits in the top 10 tokens.

Think about how extreme that is.

In the stock market, concentration among the largest names is enough to drive returns. In crypto, the concentration is even more severe. The market has effectively already told you where most of the value is being stored.

So if someone’s portfolio is heavily tilted toward random small caps, old losers, or illiquid “comeback” plays while underweight Bitcoin and the largest assets, they are not really following the evidence. They are making a very specific speculative bet that the dead or forgotten names will revive and outperform the established winners.

That can happen occasionally. But as a default portfolio construction method, it is weak.

What the data suggests for crypto portfolio construction

To be clear, this is not a prescription for what anyone must buy or hold. Crypto is extremely risky, and most things fail.

But if you are trying to take lessons from long-run market behavior, the implications are hard to ignore.

Three ideas stand out:

- Concentration risk is often overstated. Markets naturally concentrate around the strongest assets and protocols.

- Winners tend to keep winning. Relative strength matters more than bargain hunting in many cases.

- Selling losers and holding winners beats praying for mean reversion. Down bad is not the same thing as undervalued.

For many crypto portfolios, this creates an uncomfortable question: why are they not anywhere close to market-cap weighted?

If Bitcoin represents around 70% of the economic weight of the token market, most portfolios are dramatically underweight it. That may be fine if the goal is aggressive speculation. But if the goal is aligning with how long-run winners typically behave, the mismatch matters.

And this is especially relevant during bear markets. Bear markets are when portfolios get emotionally rebuilt around hope instead of evidence. People become attached to what has fallen the most, because it feels like upside. But history suggests the smarter exercise is asking: which assets are still proving they deserve to lead when the cycle turns?

You do not need to pick the unicorns early

One of the most freeing ideas in all of this is that you do not necessarily need to find the future Amazon or Nvidia before anyone else.

You just need exposure to the winners when they become winners.

That is what rebalancing and market-cap weighting effectively accomplish. They let the market reveal the leaders, and then they increase your exposure to those leaders as they prove themselves.

This is a very different mindset from trying to be the smartest person in the room with obscure picks. It is more humble. It assumes you do not know in advance which projects will dominate, so you let market structure help make that decision over time.

That does not eliminate risk. Nothing in crypto does. But it is a more evidence-based way to think about the game.

Where trading signals fit into a market like this

For anyone actively trading around these trends rather than simply holding a long-term portfolio, structure matters just as much as conviction. In a market where leadership can rotate fast, and where most smaller tokens never recover once they lose relevance, good analysis becomes far more important than chasing noise.

That is exactly why many traders look for best crypto trading signals that focus on momentum, risk management, and market structure instead of social media hype. In a concentrated market, the biggest edge is often not finding a hidden gem. It is recognizing which leaders are strengthening, which losers are breaking down, and where capital is actually flowing.

Signals are not magic, obviously. They are tools. And like any tool in crypto, they should support a process, not replace one. If you are using them, it is worth understanding both the benefits and the limitations, which is why this overview of the pros and cons of using crypto signals for trading is useful context.

Why this thesis pushes many people back toward Bitcoin

The more you think through this framework, the more radical the conclusion starts to sound.

If market returns are driven by a tiny set of winners, and if crypto is even more failure-prone than equities, and if Bitcoin still dominates the asset class by a massive margin, then it is not crazy to ask whether most people simply need far more Bitcoin than they currently hold.

That is not an anti-altcoin argument in absolute terms. There will almost certainly be winners beyond Bitcoin. There already are. Ethereum has carved out its own place. Other protocols may continue to capture value.

But if your portfolio is built as though dozens of fringe tokens will all eventually make it, the historical odds are not on your side.

The market does not usually reward broad exposure to everything. It rewards exposure to the handful of things that matter.

Stablecoins, exclusions, and why definitions matter

One nuance worth noting is that this framework looked at crypto largely through the lens of tokens excluding categories like stablecoins and certain non-comparable assets. That matters because stablecoins serve a different role in the ecosystem. They are more about liquidity, settlement, and payments than upside capture.

If you want a clearer understanding of how those assets fit into the market, this explainer on what stablecoins are and how they work adds helpful context.

But once you narrow the field to tokens competing for network value and investor capital, the concentration becomes very hard to ignore.

The real takeaway

The headline is not just that a concentrated top-10 strategy beat Wall Street for 56 years.

The real takeaway is why.

Markets are not democracies. They are power laws.

A tiny number of assets create most of the value. The broad middle underwhelms. The bottom fails. And portfolios that overemphasize laggards while underweighting proven leaders often end up optimized for storytelling, not returns.

That lesson is visible in stocks. It is probably even more important in crypto.

So the uncomfortable question is not whether concentration feels risky.

It is whether avoiding concentration in a market dominated by a few winners is actually the bigger risk.

FAQ

Why did the top 10 stocks outperform the S&P 500?

Because long-term market returns are highly concentrated in a small number of exceptional companies. A top-10 strategy keeps exposure focused on those dominant businesses instead of diluting returns across hundreds of weaker names.

Does concentration automatically mean higher risk?

Not necessarily. Concentration can increase risk in some cases, but global market history shows that concentrated markets are common and do not reliably predict poor future returns. The key distinction is whether the concentration is in strong winners or weak speculative bets.

How does this idea apply to crypto?

Crypto is even more failure-prone than stocks, which suggests returns may be even more concentrated among a tiny number of assets. Since Bitcoin and a few other large tokens make up most of the market’s value, a portfolio heavily skewed toward small, struggling tokens may be fighting both the data and the market structure.

Is buying beaten-down altcoins a bad strategy?

It can be. A large drawdown does not guarantee recovery. Many assets that fall sharply never return to former highs. Historical market behavior suggests that holding winners and cutting losers is often more effective than assuming every laggard will rebound.

Should a crypto portfolio be mostly Bitcoin?

The data discussed here points to Bitcoin’s dominant role in the crypto market, especially when looking only at tokens. That does not mean every portfolio should be mostly Bitcoin, but it does suggest many portfolios may be far more underweight Bitcoin than the market structure itself would justify.

Can crypto trading signals help in a concentrated market?

They can help if they are used as part of a disciplined process. In a market where capital tends to flow toward clear leaders, strong crypto trading signals can help identify momentum, manage risk, and avoid getting trapped in weak assets that are losing relevance.

None of this is financial advice. It is just a much sharper way to think about where returns actually come from, and why simple portfolio construction often beats clever narratives.

{kind=link}